65 / 116

65 / 116

March 18-March 31, 2015 —

COLORADO REAL ESTATE JOURNAL

— Page 5B

T

he senior care industry

recently has seen

increased interest from

outside investors, developers,

and debt and equity providers.

The specific reasons may vary

by participant but, broadly

speaking, this increased interest

is driven by an asset class

risk profile that has gained

acceptance by the capital

markets, more so today than in

previous years.

The senior care asset class

is piquing interest, fueled

by a lack of opportunities in

other commercial real estate

areas, such as office and retail,

combined with the favorable

demand demographics of

senior care. The result is a

real estate-based asset class

that has outperformed other

property types over the past

decade. As diversified investors

reach for the efficient frontier,

senior care is an asset class that

remains largely uncorrelated

to the broader market and

with relatively low volatility.

These attributes are appealing

for investors and are driving

demand for senior care assets.

Asset Class Risk Profile

It is important to first define

how the capital markets view

the senior care asset class. For

the purposes of this discussion,

we will focus on risks at the

individual site level. Through

this lens, two main categories of

risk emerge – operational risk

and financial risk. Given the

range of business complexity

and resident profiles, it would

be imprudent to develop a one-

size-fits-all risk profile for the

asset class.

Spanning the financial

risk spectrum, the various

stages of a senior care asset’s

business lifecycle include new

construction, stabilization,

turnaround and acquisition.

Further, subdividing the asset

classes into continuing care

retirement community, skilled

nursing facility, assisted living

or Alzheimer’s care, and

independent living allows

us to categorize operational

risk across the revenue types,

acuity levels and business

complexity. In total, this gives

us 16 characterizations across

the asset class around which we

can develop and subsequently

assign quartile ratings and

benchmark metrics.

Each site is assessed relative

to its characterization

benchmark metrics and

assigned a risk profile. The

site-specific risk profile dictates

the capital mix and the cost of

capital available to owners and

operators to meet their own

strategic objectives.

Lower Cost of Capital

Driving Valuations

The appetite for portfolio

holders and outside investors

(diversified participants) to

own senior care assets resulted

in higher valuations and, in

some markets, record-breaking

valuations. This begs the

question – are these valuations

excessive and the result of a

lack of investment discipline, or

are these valuations justified?

In order to make a proper

assessment, we can compare

cap rates to the cost of capital

of the diversified participants.

For the most part, all

participants have access

to the same senior debt

financing vehicles, such as

agency financing via the

U.S. Department of Urban

Housing and Federal Housing

Administration, or Fannie Mae.

The true advantage comes from

access to a lower cost of equity.

As valuations stretch and cap

rates decline, equity financing

is needed to fill capital gaps

required in transactions.

Outside participants and

large portfolio holders have a

distinct advantage on this front

because they have a lower cost

of equity. This lower cost of

equity is achieved because they

are more diversified, either by

geography or asset class.

The cost of equity, using

the capital asset pricing

model, ranges from 3.1 to

4.8 percent for diversified

participants. Comparatively

speaking, owners and operators

of smaller portfolios and

single assets have a higher

cost of equity from 10 to 15

percent. This is typical for

entrepreneurs who may have a

significant portion of their net

worth invested in senior care

assets and are not as diversified.

When the capital asset

pricing model is applied to

a transaction where loan to

value is 80 percent and cost of

debt is 4 percent, it translates

to a weighted cost of capital

of approximately 4 percent

for the diversified participant

and 5.2 percent for the less

diversified participant. The

lower cost of capital allows

the diversified participant to

lower its hurdle rate while

maintaining a similar risk

premium. The effect is higher

asset values due to the lower

cost of capital.

Does this mean risk

premiums will remain stable

indefinitely? The answer to

this question remains to be

seen. Historically, the data

leads us to believe that as more

diversified investors enter the

market, the stability of the risk

premium may come under

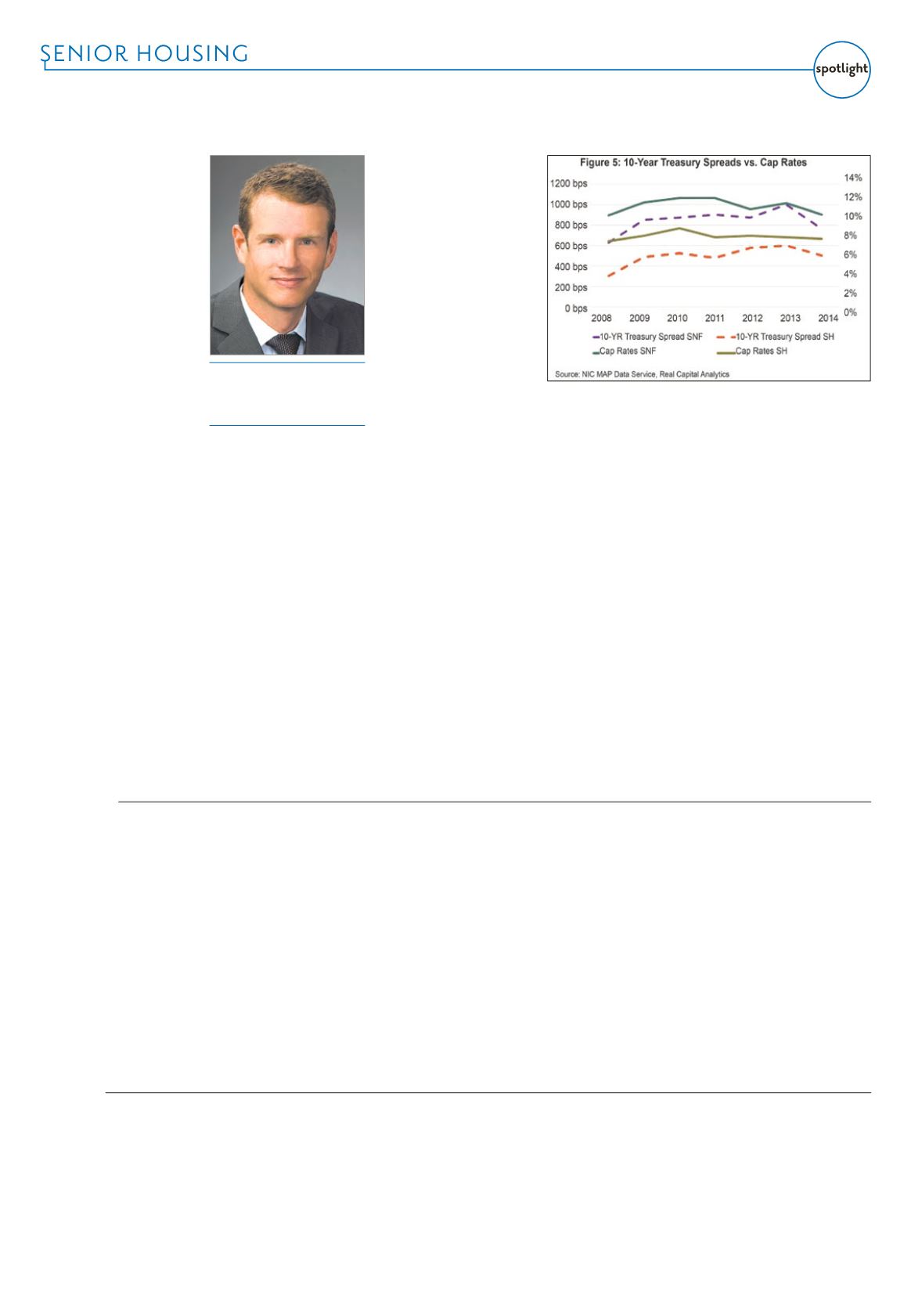

pressure. The chart shows a

tightening of spreads between

the 10-year Treasury and cap

rates of skilled nursing facilities

and senior housing. As one can

see in the table above, spreads

are tightening while cap rates

remain even. It is unclear

as to whether shrinking risk

premiums are causing spreads

to tighten or if the asset class is

becoming even less correlated

to the overall market.

Generally, the acceptance

of senior care as an asset

class is a positive trend for

an industry that relies on a

variety of financing structures

to achieve strategic objectives.

This is good news for the

less diversified participants

as they have the option of

either continuing to realize

the rewards of owning and

operating a senior care asset or

divesting their asset in a more

robust and liquid market with

growing valuations.

The new must-have asset class for senior careMatt Lindsay

Senior vice president, Lancaster

Pollard, Columbus, Ohio

Authority. Developers include

a mix of for-profit developers,

nonprofit developers and local

housing authorities. Some for-

profit developers with new or

under-construction affordable

properties include Hendricks

Communities, The Burgwyn

Co., Koelbel and Co., Atlantic

Development, McDermott

Properties, Legacy Senior

Residences, Wazee Partners

and MEJansen Development.

Housing authorities with new

senior apartments include

Aurora Housing Authority,

Metro West Housing Solutions,

Boulder Housing Partners,

Longmont Housing Authority,

Jefferson County Housing

Authority and the Denver

Housing Authority. Two

nonprofit organizations,

InnovAge and Accessible Space

Inc., opened new buildings in

Thornton and Greeley.

So, given all that is already

in the development pipeline,

is there remaining opportunity

and, if so, where is it? The

answer is a selective yes, if it is

the right product type in the

right location.

It is clear that current

development is concentrated

in certain housing and care

facility types, and is unevenly

dispersed geographically.

Regarding housing and care

facility types, most of the

units under development or

recently opened are either

assisted living or memory care.

Development of independent

living apartments has been

slower to return since the

end of the recession, with

only a modest resurgence

of development underway.

The newest independent

living facilities to open have

done very well, and there is

additional demand in many

geographic areas. Finally, a

number of skilled nursing

facilities, primarily focused

on short-term rehabilitation

patients, recently opened

or are underway in metro

Denver, Colorado Springs and

Grand Junction – and there

is probably more demand in

other markets within the Front

Range.

Looking at specific

geographic markets, some

areas with the highest

volume of new development

are the southeast Denver

metro area and southeast

Aurora, the Broomfield and

Westminster area and the

northern portion of Colorado

Springs. Yet, even in those

areas, the communities under

development are limited to

certain types and there may be

additional demand for other

products. For example, most

of the current development in

Broomfield and Westminster

is limited to assisted living and

memory care.

Opportunities are there if

you do your homework to

find a strong and underserved

market, and then plan the

right project with a high-

quality team. But, be sure to

understand what is already in

the pipeline, as many projects

are underway or about to open.

Boom Continued from Page 15AAfurther delay the licensing

process.

Medicaid Certification

The Colorado Department

of Health Care Policy and

Financing administers the

Colorado Medicaid program

for assisted living residences.

A Medicaid-certified assisted

living residence is known as

an alternative care facility. The

current operator must provide

notice to HCPF at least 30 days

prior to the anticipated change

of ownership date and the

new operator must submit a

separate Medicaid application

with HCPF. There is no option

for an alternative care facility

to assign an existing Medicaid

provider agreement, and the

new operator cannot bill under

the prior operator’s Medicaid

provider agreement if an

assisted living residence license

is issued, but the Medicaid

change of ownership process is

not complete. A new operator

cannot bill for Medicaid

services until the Medicaid

application has been approved

and a new Medicaid provider

agreement has been entered

into. The effective date of

the Medicaid approval can be

retroactive to the effective date

of the assisted living residence

license. So, there can be a

delay in receiving Medicaid

payments if a Medicaid change

of ownership is not processed

in a timely manner.

Both the licensing and

the Medicaid certification

processes can take a significant

amount of time to complete.

DPHE will make every effort

to process the health facility

application as quickly as

possible, but with limited

resources DPHE cannot always

expedite the processing of

a license application. There

are a number of factors that

could substantially increase

the time needed to process

the assisted living residence

license application, including

issues that arise from the

fitness review, obtaining local

jurisdiction or DFPC sign-offs.

If a new operator is

considering applying for a new

Medicaid provider agreement,

the operator must plan

ahead and file the Medicaid

application and supporting

documentation sufficiently

in advance to minimize the

period of time that it will not

be able to bill the Medicaid

program.

Lead Continued from Page 16AA