10 / 100

10 / 100

Page 10 —

COLORADO REAL ESTATE JOURNAL

— February 18-March 3, 2015

Your trusted resource in creating a vibrant vision for

your Senior Living Project —we will help you from

Concept

to

Design

to

Operation

.

Management

Consulting

Development

We’re your innovative and

comprehensive resource:

• Demand projections and financial modeling

• Development and design consulting

• Resource for architects, lenders,

developers and providers

• Third party operator/manager

• Operational assessments

• Census development

With more than 40 years in the senior living

industry, contacting us simply makes good sense:

info@clsmail.org or

720.684.4600

.

DiscoverCLS.orgGreater Denver

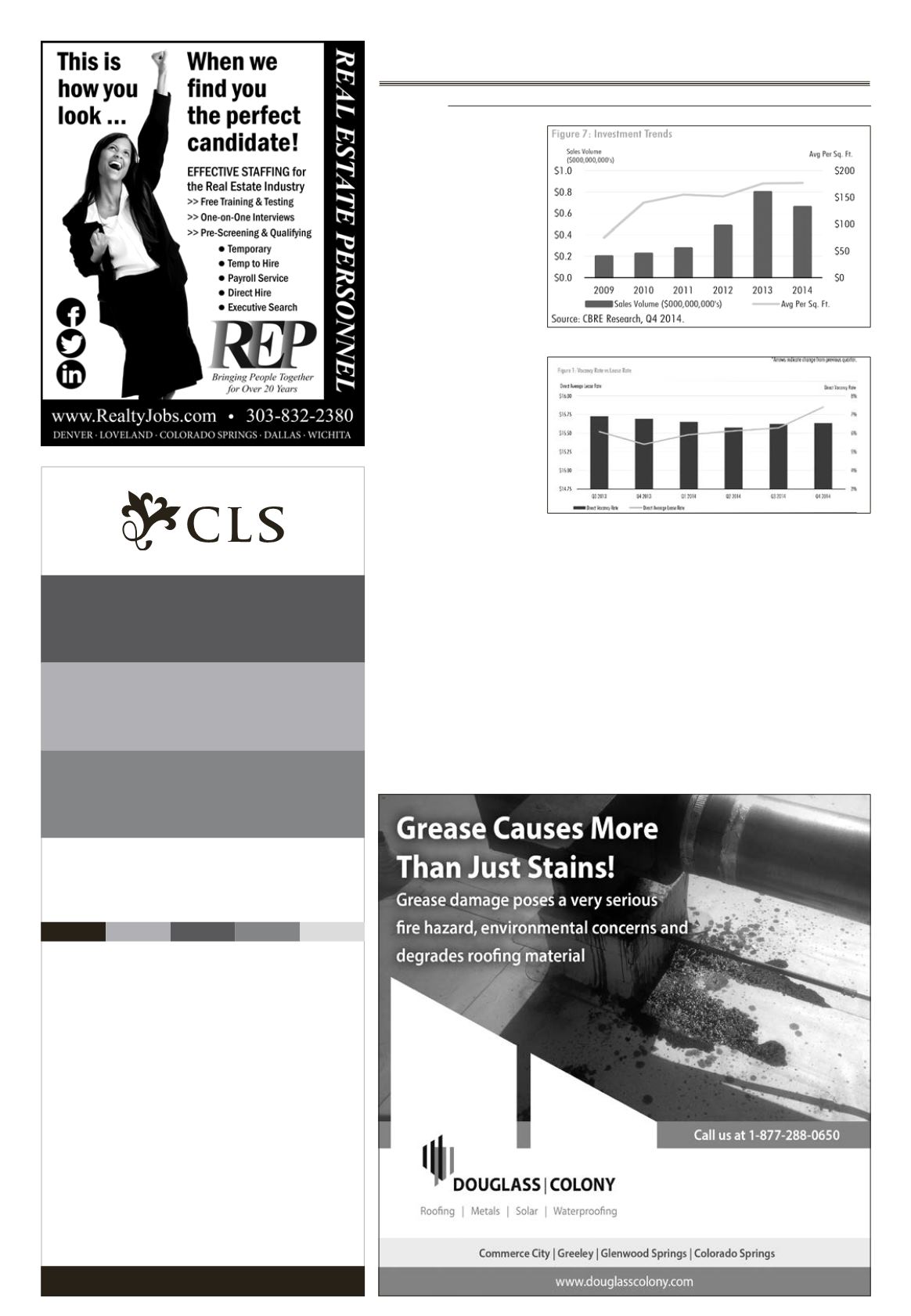

“What I would tell you is that

2013 was one of the most active

markets we have ever seen in

recent memory,” Lyons said.

“We sold a lot of stuff,” he said.

“When it came to 2014, we had

soldsomuchstuff in2013 therewas

just not that much left to trade.”

In 2013, investors were search-

ing for assets that provided a high

yield.

“Bonds were expensive, interest

rates were low and it was the per-

fect time to invest in real estate,”

Lyons added.

Lyons said based on discussions

with colleagues across the country,

Denver followed national trends in

both 2013 and 2014.

“Every market across the coun-

try slowed in 2014 from 2013 and

Denver was no exception,” Lyons

said.

For sellers, the benefit of the

shortage of properties was that

prices were higher.

“Last year, we saw record-low

cap rates on a number of assets,”

Lyons said.

He said cap rates fell “pretty

much across the board,” whether

they were for grocery-anchored

centers, large destination retail cen-

ters or strip centers.

“On just about every one of our

offerings we received multiple

offers,” Lyons said.

He said that he expects more of

the same in 2015, with the excep-

tion that occupancy levels will rise.

At the endof last year, the overall

vacancy ratewas 6.5 percent, about

the same as at the end of 2013,

according to CBRE.

“Given that there is not that

much construction underway, I

would expect occupancy rates to

rise this year,” Lyons said.

Rental rates also will continue to

rise, especially in strong markets,

such as near ParkMeadows, Cher-

ry Creek, along the U.S. 36 corridor

and in Boulder.

“It goes without saying that

downtown Denver will also do

well this year,” Lyons said.

“There is a lot happening in

LoDo and around Union Station,

which is generating a lot of buzz,”

Lyons said.

Indeed, CBRE pointed to the

announcement that Whole Foods

will open a 56,000-square-foot store

in downtown as one of the retail

highlights of last year.

The Whole Foods will be the

retail anchor for the Class A 17W

apartment community being

developed by the Holland Prop-

erty Group.

One thing that hasn’t yet

boosted retail sales in Colorado

or the nation is low gas prices,

Lyons said.

He noted a “disappointing”

national retail report that was

released in mid-January.

“When we sit down and talk

to retailers and investors, they

think it will take some time for

low gas prices to trickle down

to consumer spending,” Lyons

said.

“People don’t seem to be

using their excess discretionary

dollars to go out and buy a new

TV or a new car. At least not yet.

That is something we are keep-

ing our eyes on.”

s

CBRE Continued from Page 4Graph showing retail sales volume and lease rates in the Denver area

Graph showing retail lease rates and vacancy rates