December 17, 2014-January 6, 2015 —

COLORADO REAL ESTATE JOURNAL

— Page 23

Law & Accounting

O

n Oct. 31, 2014, the

Treasury Department

issued proposed regu-

lations that would amend exist-

ing regulations and the manner

in which ordi-

nary income

is potentially

re c ogn i z ed

upon distribu-

tions of cash or

property to a

partner. While

the proposed

regul at ions

currently are

not manda-

tory, they may

be relied on

beginningDec.

3, 2014, offer-

ing another

option for the treatment of affected

distributions.

The proposed regulation prin-

cipally relates to Internal Revenue

Code Section 751; this sectionorigi-

nally was enacted in 1954 andwas

intended to prevent conversion of

ordinary income into capital gain

and shifting of ordinary income

among partners in a partnership.

The rules apply toboth the sale of a

partnership interest from one part-

ner to a new or existing partner

and to distributions from a part-

nership to a partner, whether or

not in liquidation of the partner’s

interest. In general, a partnership

interest is a capital asset, similar

to a share of corporate stock, and

upon its sale or upon certain dis-

tributions, gain would be consid-

ered as a favorable capital gain. To

the extent the partnership owns

unrealized receivables or appreci-

ated inventory (Section 751 assets),

however, the gain potentially is

recast as ordinary income to any

partner who has a reduction in his

or her share of Section 751 assets.

The proposed regulations simplify

howthispotential ordinary income

piece is measured and determined

for distributions by a partnership.

The rules would not materially

change the determination of the

ordinary income element upon the

sale of a partnership interest by a

partner.

The proposed rules generally

will affect adisproportionatedistri-

bution to one partner. That could

be disproportionate in amount

or in composition of the distribu-

tion between cash and property.

In order for the rules to apply, a

partnership must own Section 751

assets. As noted above, a Section

751 asset for this purpose is either

of the following:

n

Unrealized receivable –

the

simplest example is an account

receivable for services provided

by a cash-basis taxpayer, although

there are a number of other items

statutorily defined as an unreal-

ized receivable for this purpose.

n

Appreciated inventory –

inventory is deemed appreciated

if its value ismore than 120 percent

of its adjusted basis.

The approach adopted in the

proposal assumes each partner

owns a share of the Section 751

assets. Under that assumption, if

any partner has a reduction in his

or her share of the partnership’s

Section 751 assets from immedi-

atelybefore adistribution to imme-

diately after the distribution, that

partner will have ordinary income

to the extent of the reduction. One

of themost important changes con-

tained in the proposed regulations:

Immediately before the distribu-

tion, the assets of the partnership

are revalued under existing 704(b)

regulations. The effect of the reval-

uation and the interrelationship of

Section 704(c) is to lock each part-

ner’s share of the Section 751 assets

to his predistribution allocation,

regardless of ownership or sharing

percentages after the distribution.

The following example illustrates

the concepts of a partner’s share of

Section 751 assets and the revalua-

tion rule:

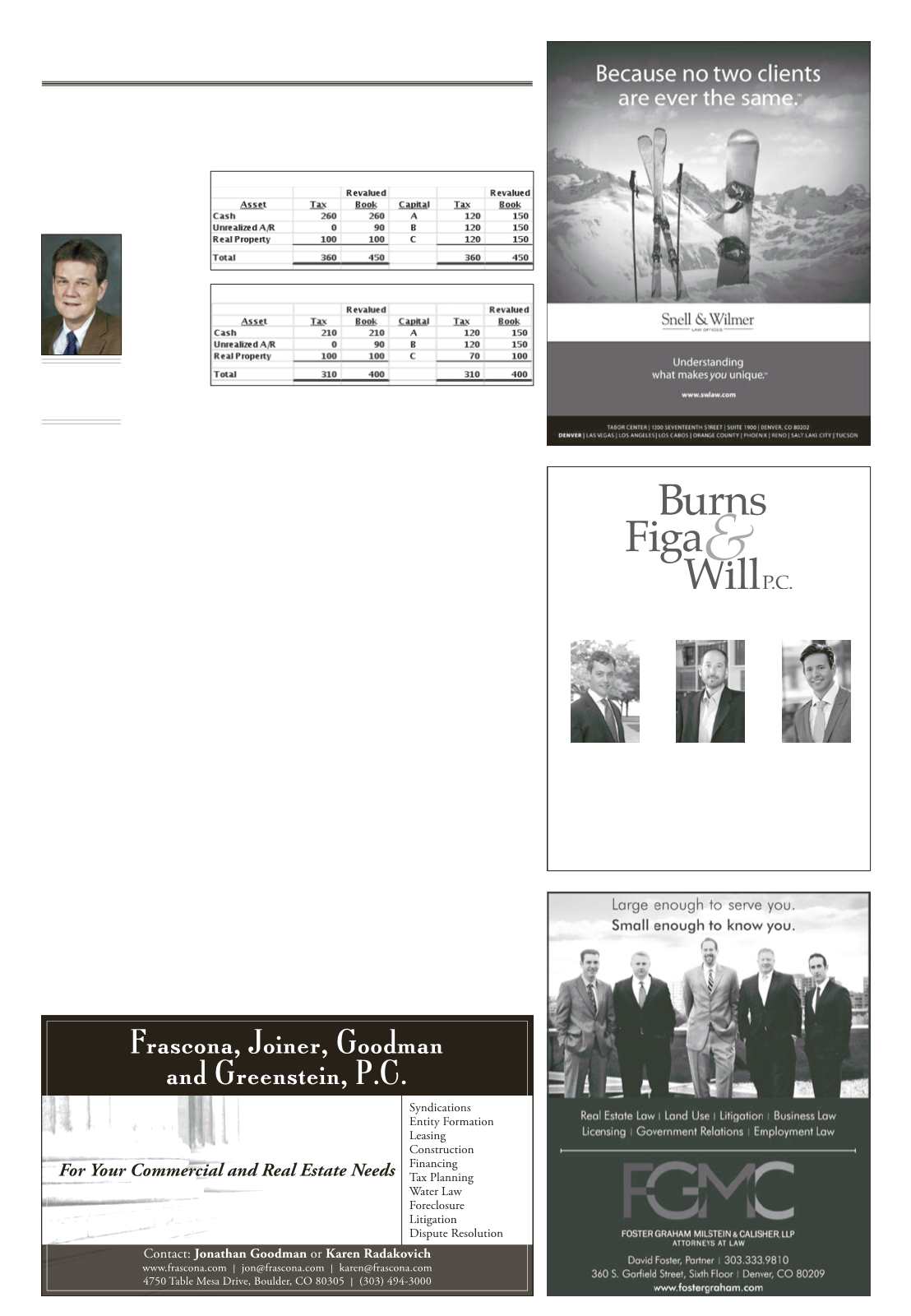

In ABC Partnership, Example 1,

Partner C wants a $50 cash distri-

bution. Each partner’s share of the

Section 751 asset is $30 – one-third

of its $90 value.

Upon receipt of the $50 cash dis-

tribution, C becomes a 25 percent

partner and the balance sheet of

ABC Partnership is depicted in

Example 2.

To determine if the distribution

caused ordinary income to any of

the partners, compare each part-

ner’s share of Section 751 assets

before and after the $50 distribu-

tion to Partner C. Due to the man-

datory revaluation, each partner

has a $30 share both before and

after; therefore, none of the $50

distribution to C is taxable. If the

revaluationdidnot occur, Cwould

have recognized $7.50 of ordinary

income on the distribution – the

decrease in C’s $30 share of the 751

asset before distribution and his

$22.50 (25 percent) share post-dis-

tribution. The $30 ordinary income

allocation to C is preserved by the

reverse 704(c) rules and will be

recognized by C when the unreal-

ized receivable is recognized for

tax purposes.

While these proposed rules

would require additional com-

pliance time and capital account

tracking, they provide the oppor-

tunity to defer ordinary income

recognition by one or more part-

ners in the case of disproportion-

ate distributions by a partnership,

subject to certain anti-abuse rules.

While seemingly complex in some

regards, the proposal is generally

a welcome relief in its simplic-

ity and practicality compared to

the existing rules. The proposal is

not without quirks and unwieldy

provisions, but as they are only

proposed, Treasury has requested

comments on ways to make the

proposed rules more workable in

their application.

Contact your financial adviser

for more information on how

these changes could affect you.

This article is for general informa-

tion purposes only and is not to be

considered as legal advice.

s

Tad A.

Goodenbour,

CPA

Partner, BKD LLP,

Colorado Springs

6400 S. Fiddler's Green Circle

Suite 1000

Greenwood Village, CO 80111

Phone (303) 796-2626

Fax (303) 796-2777

Deals. Litigation. Great Service.

Merc Pittinos

Matt Dillman

Abe Laydon

Attorneys at Law

Example 1

Example 2