6 / 28

6 / 28

Page 6

— Retail Properties Quarterly — August 2017

www.crej.comState of Retail

Great Opportunities Available inWestern Centers’ Portfolio

t

t iti

il l i

t

t ’

tf li

To schedule a showing at one of Western Centers’ 20 Shopping Centers

or for assistance in locating a new space for your business, please contact:

Corey R. Wagner

(303) 676-8211

corey@westerncenters.comGarrett Walls

(303) 676-8206

garrett@westerncenters.com303-306-1000 | 10555 E Dartmouth Avenue, Suite 360, Aurora, CO 80014 |

www.westerncenters.comFoothill Green, Littleton

Join new anchor, e Lucky Mutt, in one

of the few inline spaces available

Havana Exchange, Aurora

Excellent free-standing building and two

inline space available

Mission Trace North, Thornton

Rare opportunity of 16,000 sf junior anchor

space available at one of the State’s busiest

King Soopers anchored centers, plus four

other inline spaces available

Colfax/Wadsworth, Lakewood

10,000 sf anchor available now with opportunity

to incorporate brand into remodel of center

Cottonwood Square, Parker

Adjacent to King Soopers Marketplace, high

visibility end-cap and inline space available

Village Square, Brighton

Join Bomgaars, Dairy Queen (under

construction) and Specialized Physical

erapy, in the nal inline space available

W

hile high-profile, big-box

store closures and Ama-

zon’s announcement of its

acquisition ofWhole Foods

fuel the narrative that brick-

and-mortar retail is coming to an end,

a deeper inspection of retail property

performance from a macro perspec-

tive suggests that the predictions of the

looming demise are greatly overstated.

Stable employment growth and rising

wages bolstered consumer spending in

May to 13 percent above the all-time,

inflation-adjusted high recorded in

2008.

Although e-commerce sales contrib-

uted significantly to this figure, this

shouldn’t be understood as the end of

retail, but rather as the beginning of a

new phase in retail’s evolution in which

opportunity and upside still exist.This

is particularly the case in Denver where

retail property performance metrics

such as employment, vacancy and

rents fare better than their correspond-

ing national averages.

Employment growth in the Mile High

City outpaced the 1.4 percent national

rate during the year ending in the first

quarter. Hiring was led by the educa-

tion and health services sector and

the leisure and hospitality sector. By

the end of 2017, Denver employers

are anticipated to expand headcounts

by 2.1 percent. Relatedly, the median

household income has increased over

the 12-month period ending in March

to $74,400 annually, which encouraged

greater consumer spending and sup-

ported absorption, vacancy and rental

improvements of retail real estate.

Although strong retail sales continue

to generate robust tenant demand for

space, the development pipeline will be

more modest this year.

In 2016, builders

delivered 762,000

square feet of retail

space.This year con-

struction activity will

moderate slightly,

with only 714,000

sf of space slated

for completion.The

northeast and north-

west submarkets

will receive the bulk

of new retail real

estate.The majority

of new retail space,

however, is preleased and will support

strong net absorption of 1.2 million sf

of new and unutilized space in 2017.

Necessity and lifestyle retailer demand

will account for a substantial portion of

the absorption of space this year, which

also will impact vacancy.

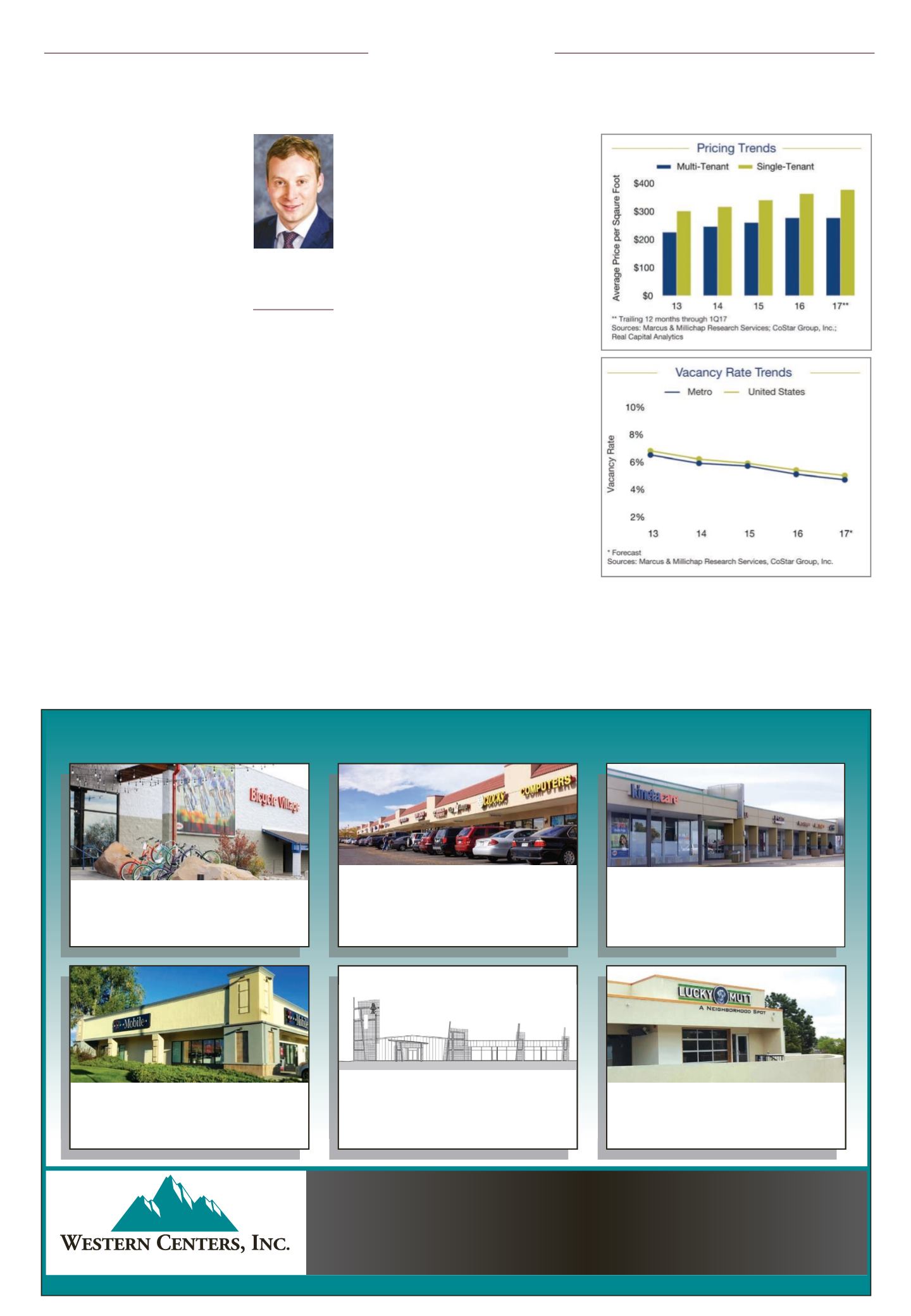

As of the first quarter, retail property

vacancy in Denver dipped to 5.1 per-

cent.Vacancy is expected to continue to

decline another 40 basis points, reach-

ing 4.7 percent by year’s end. In the

west and central submarkets, vacancy

sank below 4 percent and could fall

further as several projects for necessity

retailers including National Grocers,

CVS and King Soopers are underway.

As vacancy drops metrowide, rents are

expected to go up as a result.

By the end of the year, average asking

rents in Denver will jump a predicted

4.8 percent to $17.35 per square foot,

a new high. In the west and central

submarkets, rent growth was above the

metro average due to strong absorp-

tion.

It is worth noting that although

Denver’s economic fundamentals and

retail property performance metrics are

positive, the limited number of retail

asset listings slowed deal

flow over the 12-month

period ending in March.

In this period, deal flow

for single-tenant assets

compressed 13 percent.

Sluggish investments

sales activity was par-

ticularly pronounced

for multitenant proper-

ties, where transaction

velocity fell 23 percent.

Notwithstanding, buy-

ers were most active in

the central submarket,

where cap rates for

single-tenant assets

dropped into the low-5 to

mid-6 range. Initial yields

varied considerably, fall-

ing under 5.5 percent for

the best properties with

national credit tenants.

Higher first-year returns

were most commonly

found in peripheral sub-

urban markets.

Looking ahead, inves-

tors will scour the

market for value-add

opportunities, which

represents a wide range

of prices dependent on

tenancy, deferred main-

tenance and capital

requirements to bring

rents to market value.

Additionally, western submarkets hold

upside given that rent growth in those

areas has outpaced the rest of the

metro.

Going forward, the ability to turn the

current dynamics and negative head-

lines into new opportunities may end

up being one of the best wealth-creat-

ing strategies in retail real estate. Retail

is full of highly skilled and sophisticat-

ed owners and advisers, and those who

successfully reposition their properties

to take advantage of the market chang-

es will be poised to reap the benefits of

an industry that is a staple of American

culture.

▲

Denver market offers support for retail opportunitiesDrew Isaac

First vice president

investments,

Marcus &

Millichap, Denver