August 2015 — Property Management Quarterly —

Page 15

and 40 percent of the construction

workforce was displaced during that

two-and-a-half year period.”

Those who remained employed

saw their businesses cutting costs

to stay afloat. Many businesses were

unprepared to deal with the recession

and therefore kept costs from rising

for the following couple of years, said

Scott W. Farrell, vice president, i2 Con-

struction.

The same thing happened to the

material suppliers, most of which

were selling at or below cost for mul-

tiple years to stay in business, Hordin-

ski said.

By 2013, the industry was back to

where it was prerecession, said Far-

rell. “The issue that we started to deal

with for the first time was the lack of

labor force as they transitioned to the

oil fields in North Dakota as well as

large Davis Bacon projects within the

market,” he said.

While the market struggled to find

labor, which lost skilled tradesmen of

all types, the demand for new projects

escalated.

“The final result of the recession

was shortage of skilled labor and

unsustainable material costs, com-

bined with pent-up demand because

many customers were slow to invest

in needed capital improvements while

the macro market was so uncertain,”

said Hordinski. “The market anomaly

of costs going down for multiple years

continued for over three years. So

when the market finally got to a point

where we started seeing growth, the

contractors and suppliers first had

to catch back up to where they were

before the start of the recession.”

With the market doing well again,

vendors and manufactures began to

put a premium on their products and

people. “They are making up for lost

time,” said Farrell.

An example of this premium is

the cost of concrete. Three years ago,

Provident Construction paid in the

low $80s for a yard of concrete, said

Hordinski. After jumping almost 10

percent each year, prices were in the

mid- to high-$80s in 2013, the mid-

$90s in 2014, and now are over $100

a yard. “You can do that same anal-

ogy on a sheet of drywall, wire for an

electrician, or any type of major com-

modity that you use in the construc-

tion industry,” he said.

This year, while the market

remains strong and costs continue to

rise, contractors are reporting a slight

decrease in inflation.

“The most important concept that

I hope you can communicate is that

the costs the real estate community

and property owners were seeing five

years ago were numbers that were

not sustainable,” Hordinski said. “The

costs were driven down to a point

where virtually everyone was operat-

ing at or below cost for over multiple

years, and this current pricing is

just normalization to get back to a

sustainable market condition were

contractors and suppliers can suc-

cessfully operate over time.”

While a 3 percent increase to costs

every year is the 30-year norm, it

would be foolish not to assume a

little higher inflation throughout

the market for the next year or two,

Miller said.

Advice for Property Managers

With that in mind, when budget-

ing for tenant improvement projects,

property managers should budget as

much as 15 to 20 percent more than

they would have budgeted for the

same project in 2013, said Miller.

“It is very difficult to make general-

izations about interior construction

costs, as every project is different

in numerous ways, whether it be

materials, schedule or even payment

terms,” said Farrell. “In the past year,

I would estimate that a space that we

would have built out in May of 2014

for $45 per square foot would now

cost between $55 and $60 per square

foot.”

However, the biggest shift for

property managers may be how

they approach a project, rather than

how they budget it. There is now an

emphasis on an integrated process

that brings the contractor into the

discussion early, rather than complet-

ing a general bid process.

Prerecession, about 65 percent of

Provident’s projects were secured in

a straight negotiated fashion, 20 per-

cent were negotiated as design-assist

projects and 15 percent were hard

bids. Today those numbers have been

reversed, with 65 percent now design-

assist projects and 20 percent are

straight negotiated, Hordinski said.

“Contracting on a design-assist

method has become a lot more popu-

lar,” he said. “The primary function

for doing that is to control costs, so as

the plans are developed we’re giving

input and helping create a working

budgets to keep a project financially

on track. That has been a big change

in the marketplace.”

A good contractor can be most

helpful before a deal is finalized to

provide real time numbers and advise

as to availability of labor to complete

a project, said Farrell.

Managers will get a better deal if

they pick a contractor partner and

develop the project’s scope and price

together, rather than if the manager

goes out and tries to get 10 different

bids, Miller said. This is because the

current market demands keep a lot

of those companies from bidding for

new projects. Miller estimates that a

manager would be lucky to get bids

from half to a quarter of the general

contractors called. Most of Alliance’s

current clients use this integrated

approach rather than hard-bid

approach, he said.

If the market was still in a reces-

sion, Miller would advise differently.

When many businesses are just try-

ing to keep the doors open and a

manger solicits bids, he would prob-

ably get 11 out of 12 companies con-

tacted to bid the project, Miller said.

Additionally, property managers

should be aware of the increased

time required to receive permits

because of staffing issues in many

municipalities as well as the signifi-

cant amount of construction activity,

said Farrell.

“Finally, I would note that labor

truly needs to be treated like a long-

lead item,” said Farrell. “You can no

longer bid a project on Friday and

expect them to be up and running

the following week.”

s

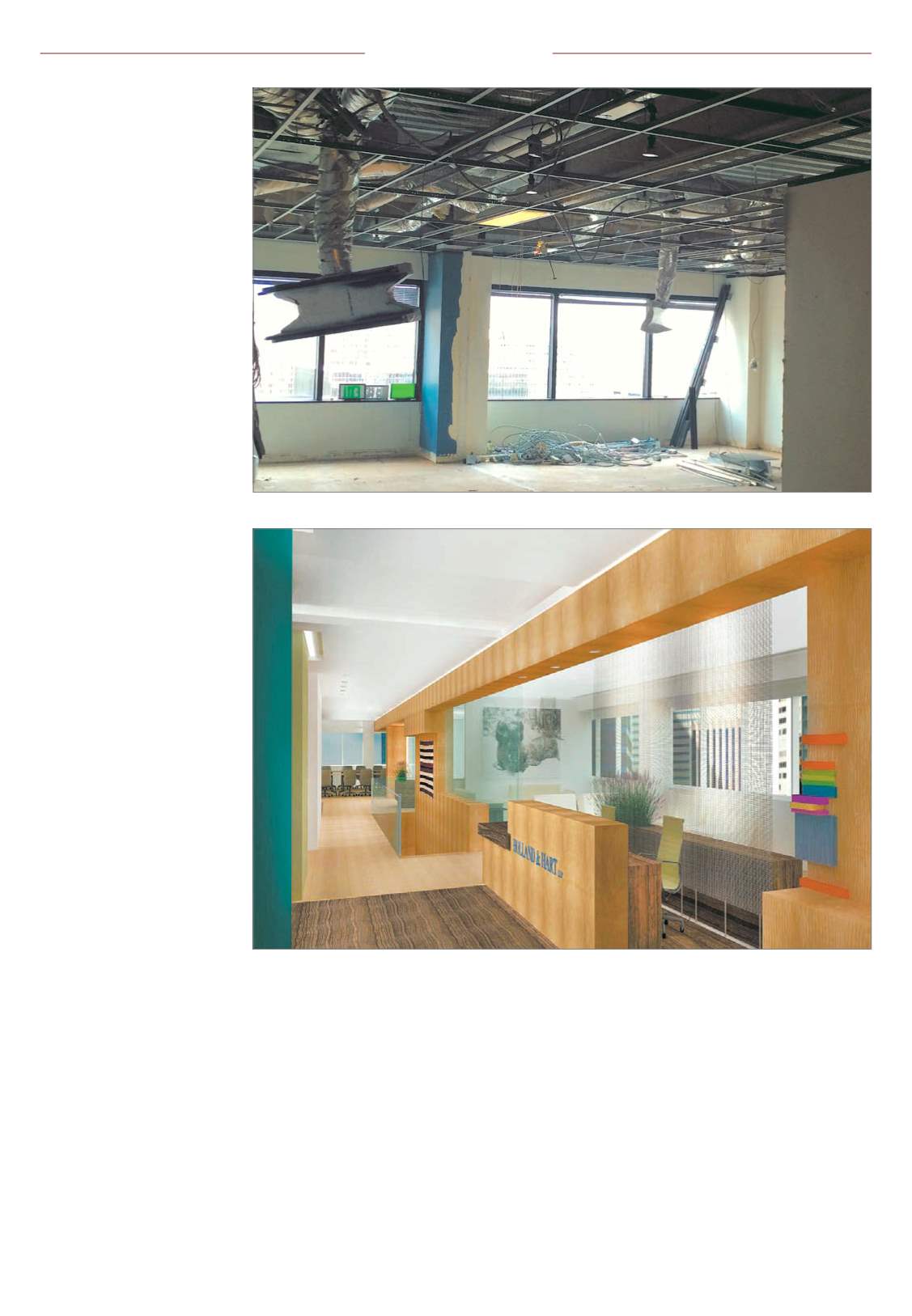

Management

Property managers are advised to bring a contractor into the discussion early for best results for tenant improvement projects.

Photo courtesy Provident Construction

While the market struggles to find skilled labor, the demand for new projects continues to escalate.