4 / 32

4 / 32

Page 4

— Office Properties Quarterly — March 2017

O

ver the last few years, Den-

ver’s office property market-

place has been bolstered by

strong hiring in the metro’s

primary office-using sec-

tors, which enabled vacancy to

hover near a decade low by midyear

2016. By year’s end, local employers

added 47,900 workers to payrolls,

10,000 of which were office-using

positions.

The office market will continue

to improve in 2017 as firms expand

into larger spaces and hiring in pri-

mary office-using sectors remains

stable. This year, area employers

will increase the Denver workforce

by 2.8 percent, or 41,500 employees.

This includes 10,000 office-using

positions, which will help offset a

robust development pipeline.

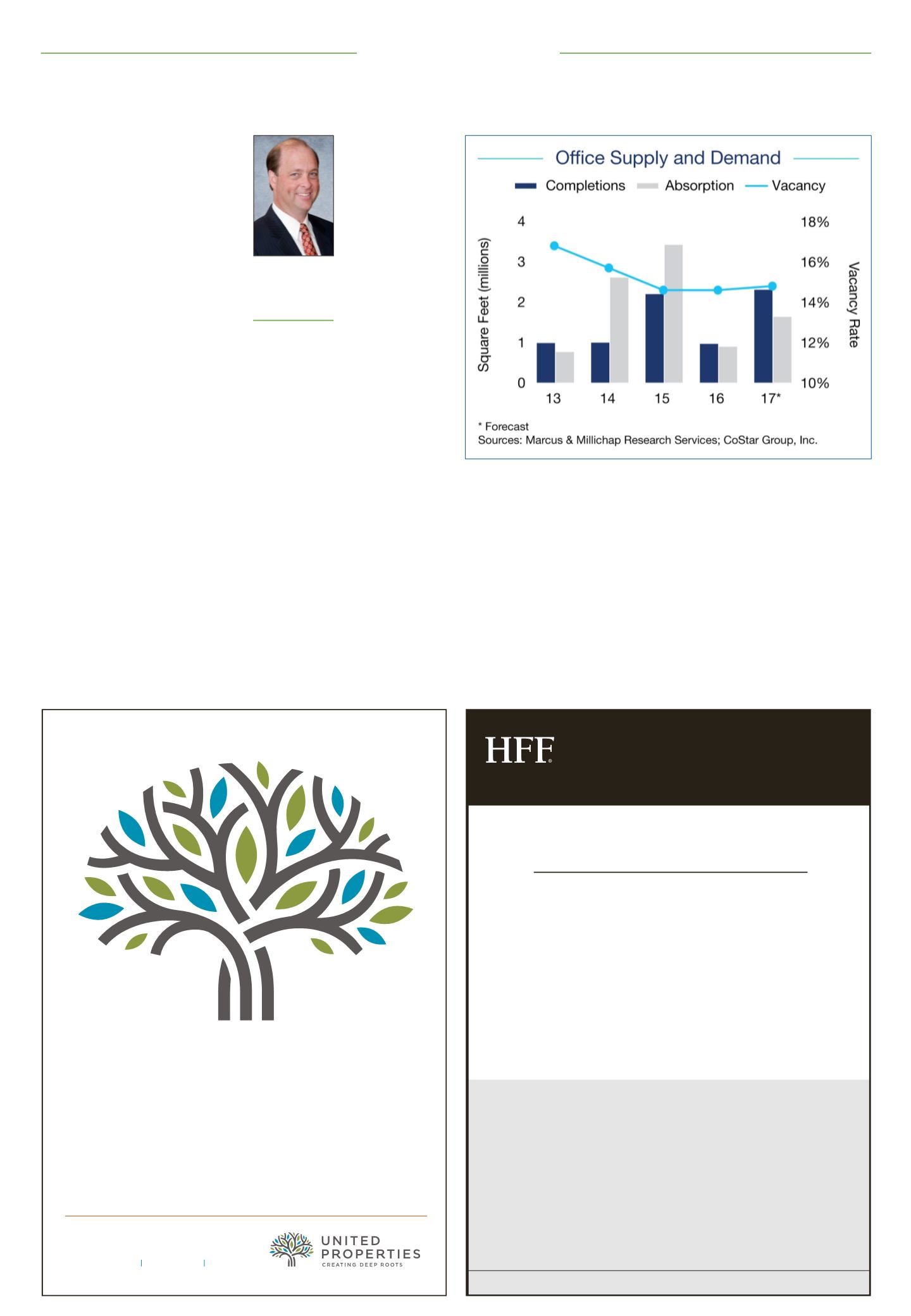

In 2016, new supply encountered

high demand throughout the Den-

ver metropolis with companies

including Comcast and Agrium

signing leases at speculative office

projects. Comcast announced that

it would move 1,000 workers into

a 212,000-square-foot building in

Centennial this year, while Agrium

moved forward with plans to con-

solidate its U.S. headquarters into

a 120,000-sf space in Loveland. One

of the largest projects completed in

2016 was the 127,000-sf FirstBank

headquarters in Lakewood. Overall,

by year’s end, builders had deliv-

ered 960,000 sf of office space to the

Denver metro area.

Developers, encouraged by several

years of relatively stable vacancy

levels and a healthy job market,

will move forward

with a number of

speculative office

projects this year

to address persist-

ing demand for

new space. Con-

struction will be

largely focused in

the downtown area

and along Inter-

state 25 through

the Denver Tech

Center, Green-

wood Village and

Centennial. Den-

ver’s commitment to providing an

expansive network of commuter rail

lines and alternative forms of trans-

portation has attracted residents

and companies to these areas.

By the end of 2017, deliveries are

projected to reach a cyclical high of

2.3 million sf of office space, a sig-

nificant increase from the previous

year.

In 2016, vacancy remained at a

historical low, ending the year at

14.6 percent. Heightened demand

for Class B/C office space dropped

the rate 40 basis points among this

asset class, while an influx of Class

A stock kept the overall vacancy

flat. The vacancy rate was lowest in

the midtown and northeast Den-

ver submarkets and highest in the

downtown submarket.

This year, healthy net absorption

will keep Denver’s office vacancy

low as completions reach their

cyclical peak; however, demand

will not outweigh the new supply.

For this reason, vacancy rates are

anticipated to rise 20 basis points in

2017 to 14.8 percent, remaining well

below the previous 10-year average.

Low vacancy last year supported

office property rent gains and

boosted the average asking rent to

$25.14 per sf, a 1.6 percent year-

over-year increase. The average ask-

ing rent growth for Class A office

space atrophied while average ask-

ing rents for Class B/C office space

surged.

In 2017, with vacancy hovering

near historical lows, the average

asking rent is forecast to rise 1.7

percent to $25.57 per sf.

Denver’s strengthening market

conditions in 2016 spurred buyer

interest in office assets, although

limited for-sale inventory hindered

transaction velocity. That said, buy-

ers targeted office properties in

southeast and southwest Denver,

along with assets in downtown and

west Denver.

2017 projected to reach cyclical high for deliveriesBrian Smith

Vice president

investments,

Marcus &

Millichap, Denver

Market Update

Marcus & Millichap

Imagining new possibilities.

Creating lasting communities.

Commercial real estate with a proven past and future focus

UPROPERTIES.COMMINNEAPOLIS DENVER

HFF DENVER

$4.7 BILLION IN 2016

$2.3 Billion

84 Debt Transactions

$2 Billion

39 Investment Sales Transactions

$385 Million

*

6 Equity Placement Transactions

2016

YEAR-END HIGHLIGHTS

For investment sales, financing, distressed debt/REO, loan sales, equity recapitalization,

restructuring services or advisory services, contact HFF.

Eric Tupler

Debt & Equity

Placement

(303) 515-8001

etupler@hfflp.comMark Katz

Commercial

Investment Sales

(303) 515-8093

mkatz@hfflp.comJordan Robbins

Multi-housing

Investment Sales

(303) 515-8010

jrobbins@hfflp.comJosh Simon

Debt & Equity

Placement

(303) 515-8002

jsimon@hfflp.comJules Sherwood

Commercial

Investment Sales

(303) 515-8027

jsherwood@hfflp.comPeter Merrion

Commercial

Investment Sales

(303) 515-8026

pmerrion@hfflp.comBrock Yaffe

Debt & Equity

Placement

(303) 515-8034

byaffe@hfflp.comLeon McBroom

Debt & Equity

Placement

(303) 515-8008

lmcbroom@hfflp.comJeff Haag

Multi-housing

Investment Sales

(303) 515-8004

jhaag@hfflp.comKristian Lichtenfels

Debt & Equity

Placement

(303) 515-8007

klichtenfels@hfflp.comChad Murray

Commercial

Investment Sales

(303) 515-8025

cmurray@hfflp.comMark Williford

Commercial

Investment Sales

(303) 515-8032

mwilliford@hfflp.com*Equity is based on total capitalization.

HFF DENVER

| 1125 17th Street, Suite 2540 | Denver, CO 80202 | (303) 515-8000

hfflp.com Please see ‘Smith,’ Page 27