Page 4

— Office Properties Quarterly — October 2015

Regulatory

T

he Dodd-Frank Wall Street

Reform and Consumer Pro-

tection Act was passed in

July 2010 and “represents

the most comprehensive

financial regulatory reform mea-

sures taken since the Great Depres-

sion,” according to The Dodd-Frank

Act: A Cheat Sheet. This article

will explore three

effects the act has

had on commercial

real estate in Den-

ver as they relate

to the financial

services sector –

lending, employ-

ment and banking.

Downtown Den-

ver’s office market

has seen impres-

sive activity in

recent years, and

there is much

to suggest these

positive trends

will continue. With

25.8 million square

feet of existing

office space and

an additional 1.8

million sf of office

space under con-

struction, Denver

is experiencing

unprecedented

growth.

One of Denver’s

largest active tenant bases is the

financial services sector. Financial

services is a dynamic industry that

encompasses a range of businesses,

including but not limited to bank-

ing, mortgage, credit card, insurance

and investment funds. In fact, Den-

ver’s 17th Street is considered the

“Wall Street of the West,” due to the

high concentration of financial ser-

vices companies.

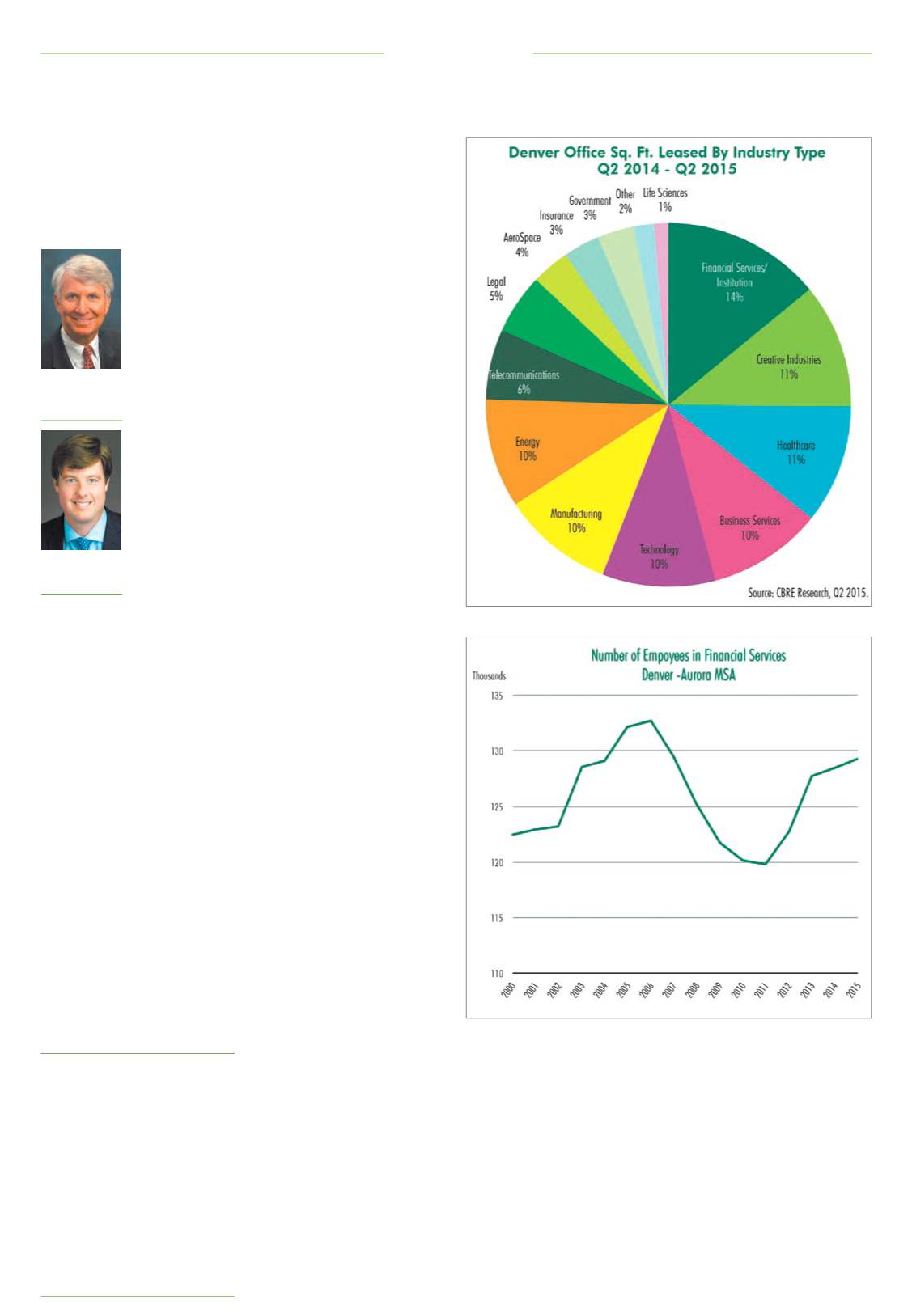

As demonstrated in the first fig-

ure, between second-quarter 2014

and second-quarter 2015, financial

services and institutional lender

tenants accounted for 14 percent of

the total space leased during this

time in Denver. This is equivalent

to more than 1.2 million sf and rep-

resents Denver’s largest sector for

office leasing activity in the past

year, according to CBRE research.

Specifically in the downtown sub-

market, financial services and insti-

tutional lending companies occupy

25 percent of Class A and AA office

space, second only to the energy

sector.

The financial services industry

largely is impacted by government

regulations and compliance. Since

the passing of the Dodd-Frank Act,

these regulations have increased.

Proponents of the Dodd-Frank Act

lauded it as “landmark legislation

that will reduce the likelihood and

magnitude of future financial pan-

ics, end taxpayer bailouts of Wall

Street and enhance consumer

protection,” according to Randall

Guynn in “The Financial Panic

of 2008 and Financial Regulatory

Reform.”

Critics predicted that the stricter

lending laws would reduce capital,

stifle employment and quicken

decline. Five years since the initial

passing, the Dodd-Frank regulations

have impacted Denver’s financial

services sector regarding lending,

employment and banking, each of

which has implications to a com-

pany’s real estate strategy.

First, the regulations implemented

impacted lending by imposing capi-

tal requirements on banks involved

in acquisition and development.

According to The Heritage Founda-

tion, the cornerstone of the Dodd-

Frank Act is a lender obligation to

determine that a borrower has the

ability to repay the loan.

This shift of accountability “pre-

sumes that consumers are incapa-

ble of acting in their own interests,”

said Diane Katz in “Dodd-Frank

Mortgage Rules Unleash Predatory

Regulators.”

Because of this, credit is much

less available to borrowers, even for

those with excellent credit scores.

What does this mean for commer-

cial real estate? Banks are making

fewer loans, thus doing less busi-

ness, which is impacting their bot-

tom line and has ramifications for

everything from hiring to office

space.

Second, with regard to employ-

ment, some speculated that the

newly imposed regulations would

have a positive impact on job cre-

ation due to increased compliance

requirements.

“These include costs of manda-

tory reporting under rules from the

new Office of Financial Research

and the Consumer Financial Protec-

tion Bureau; costs of creating and

retaining records to meet future

audit and compliance requirements;

costs of legal counsel, accountants,

and other experts for advice on

compliance and applicability of reg-

ulations; increased costs associated

with new rules for credit agency

reports and securitization require-

ments; and many others,” said Paul

Bent in “Dodd-Frank: What about

Leasing?”

In other words, more employees

would be needed to ensure finan-

cial institutions are complying with

new regulations.

Critics worried that the limited

lending as a result of restrictions

would lead to more job losses. This

is important for corporate real

estate strategy because if employ-

ment was significantly declining,

many organizations would be look-

ing to reduce their square footage

or move to less expensive areas.

Thankfully in Denver, CBRE’s

research reports the market has

seen an increase in financial servic-

es employment growth since Dodd-

Frank passed in 2010. As of June,

year-over-year growth in financial

services was 1.4 percent. Currently,

nearly 130,000 people work in the

industry and this is edging closer to

the prerecession peak of more than

135,000 financial services employ-

ees.

Finally, small banks with less

capital to fund the cost of compli-

ance may be particularly vulnerable

to the effects of this act. The risk

for small-bank failure is height-

ened due to costly implementa-

tion of new regulations, which also

restricts new bank formation and

expansion.

“Almost no new community banks

have been formed in the past few

years,” said Bill Floersch, former

CEO of ABN Amro Clearing Ameri-

cas. “This is in part due to stricter

requirements and reduced profit

potential.”

The claim that more banks failed

due to the passing of Dodd-Frank

is complicated because research

shows that the number of banks

has been steadily declining since

long before the Dodd-Frank Act,

according to a first-quarter 2015

FDIC report.

While traditional banks have

experienced a decline and this

affected their demand for office

space, new nontraditional lenders

are filling the void and pushing the

market toward surpassing prereces-

sion levels. The doors opened by

Dodd-Frank for these new lenders

may be helping financial services

absorb additional space and employ

more people in the wake of the

financial crisis.

In conclusion, a review of the

Dodd-Frank Act reveals both nega-

tive and positive implications for

commercial real estate as it relates

to the financial services industry,

and it is possible that the full effect

of the legislation will not be recog-

nized for several more years.

s

Hank Cox

Executive vice

president, CBRE,

Denver

Mark Floersch

Senior associate,

CBRE, Denver

The doors opened by

Dodd-Frank for these

new lenders may

be helping financial

services absorb

additional space and

employ more people

in the wake of the

financial crisis.