August 2016 — Multifamily Properties Quarterly —

Page 21

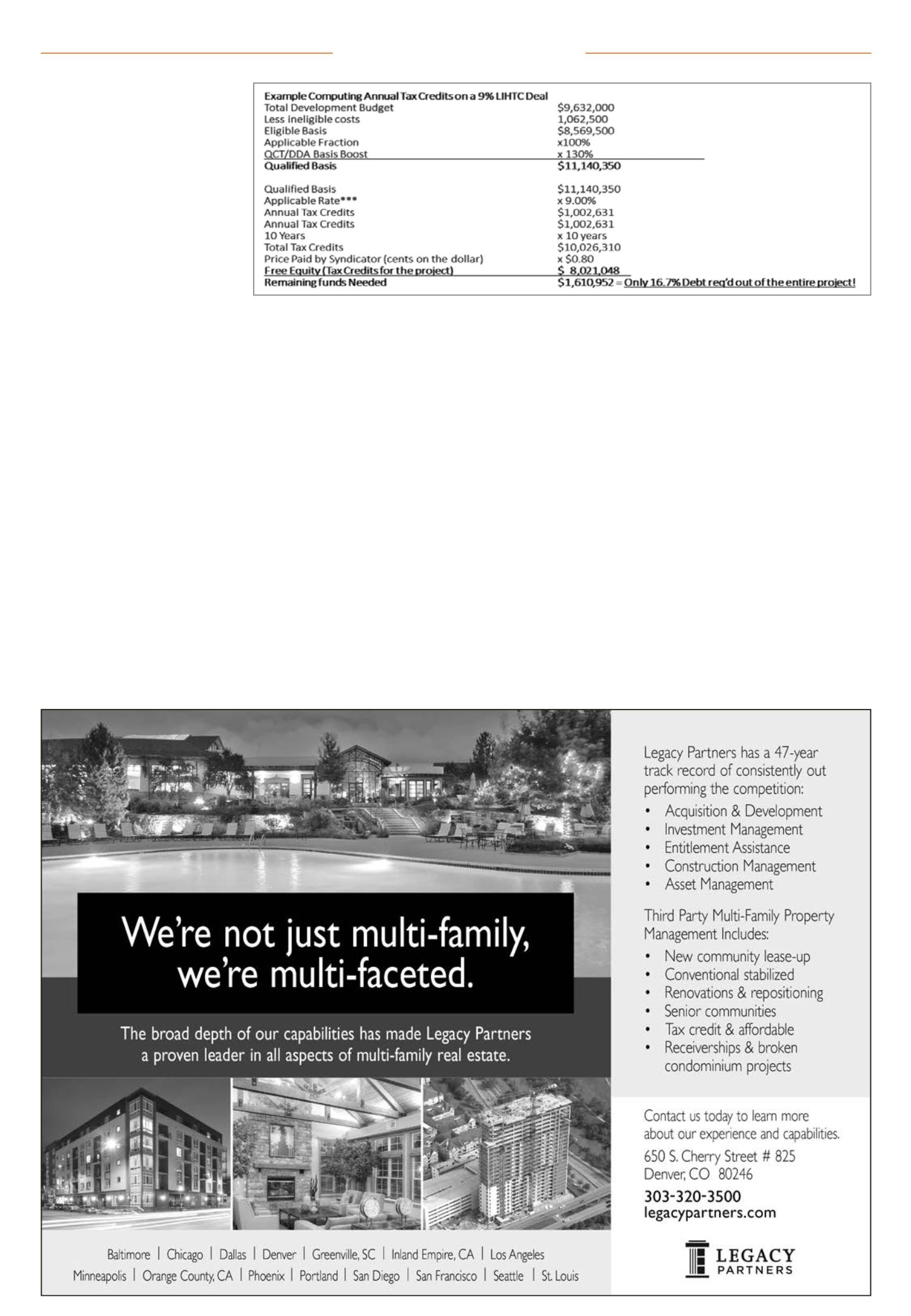

owners’ equity.

Are other funds or incentives avail-

able?

Another source of funds when

applying for LIHTC projects is the

basis boost. The basis boost increas-

es the eligible tax-credit basis by 30

percent if a project is in a qualified

census tract, a difficult-to-develop

area or a state-designated difficult-

development area. They do not

apply to tax-exempt financed proj-

ects.

The basis boost is an additional

funding source that can help a

developer overcome financial

impediments to project finance. For

example, where construction costs

may be higher, such as a market

like San Francisco or New York City,

could be a difficult-to-develop area.

It also can be used for locations

where affordable housing opportu-

nities are limited (qualified census

tract) and there is an underserved

suburban market in a good school

district versus poorer neighbor-

hoods and, thus, additional funding

incentivizes the developer to build a

LIHTC project in the area.

The following are a variety of

sources of capital for affordable

housing projects 9 percent LIHTC

and 4 percent tax-exempt municipal

bonds:

• State department of housing –

funding

• Financial institution or insurance

company (syndicator) – equity

• City/county affordable housing

funds

• Public agency housing funds

• HUD low-interest loans

• Local housing authority

• Housing choice vouchers

• Community development block

grants

• Regional employers (i.e., resorts

and factories)

• Financial institution or insurance

company – debt

What are the financial risks?

Tax-

credit projects do come with some

financial risks. The first is the

upfront costs to put together the

application for submittal to the

state. There are also costs associ-

ated with architecture, engineer-

ing feasibility, market studies, legal

counsel as well as tax and financial

consultants.

These costs can be recovered if

the applicant is successful in win-

ning a 9 percent award. However,

in a 4 percent application, while

the applicant can recover these

costs, the downside is that develop-

ers are required to piece together

other funding in order to achieve

the same 70-percent-plus funding

described in a 9 percent deal. Both

of these options require an experi-

enced design, tax and legal team.

Aren’t affordable housing proposals

fraught with neighborhood objections?

Affordable housing shouldn’t be

considered a negative land use or

only for poor people. LIHTC devel-

opments provide a much-needed

resource to our nation’s housing

stock and a diverse population. The

9 percent LIHTC project, while very

competitive, requires high-quality

design, amenities and LEED compli-

ance.

In order to receive tax credits, the

applicants are required to develop

quality projects. If either a 9 per-

cent or 4 percent tax-credit project

is properly designed, the economic

status of the residents is undetect-

able between “affordable housing”

and “market-rate housing.” In fact,

often, they are blended because of

various inclusionary housing provi-

sions embedded within local zoning

codes throughout the nation. Addi-

tionally, blending affordable and

market-rate housing diversifies the

unit mix and tenant makeup, which

improves profitability while main-

taining compliance with complex

tax requirements. For these reasons,

at least 10 percent of the units in

an affordable housing development

should be market rate to avoid com-

pliance issues if tenants understate

earnings for AMI compliance.

The parties in a tax-credit syndi-

cation work together with the State

Housing Finance Agency, acting as

the compliance entity that approves

the eligibility of the tax-credit appli-

cation as well as ongoing review of

a developments annual compliance

with property management, tax

reporting, adhering to tenant AMI

rules and associated Department of

Housing and Urban Development

rules.

The typical cast of actors in a

LIHTC deal often are much like a

Affordable Housing

LAI Design Group

The same process applies in developing a 4 percent low-income housing tax credit deal. The remaining 40 to 50 percent of funds come

from the Community Development Block Grant program, local housing authorities and other sources with debt making up the remain-

ing 20 to 30 percent balance of funds needed to finance the development.