Page 28

— Multifamily Properties Quarterly — May 2016

Pinnacle Real Estate Advisors

Matthew Ritter • Jeff Johnson

Joe Hornstein • Jules Hochman

Josh Newell • Matt Lewallen

Kevin Calame • Greg Breslau

Cody Stambaugh • Peter Sengelmann

Connor Knutson • Robert Lawson

Jim Knowlton • Scott Fetter • Brent Hubbell

Thomas Graeve • Justin Brockman

Unique Properties Inc.

Marc S. Lippitt • Scott L. Shwayder

Tim Shunta • Jason Koch • Adam Riddle

Kevin Higgins • Ryan Floyd • Alfonso Avila

Mike Hesse, CCIM

Marcus & Millichap

Greg Price • Brian Haggar • Clayton Primm

Eric Schierburg • Jason Steele • Nick Steele

Moran & Company

David Martin • Pamela Koster

FarrellRes

Frank Farrell

FarrellRes

J & B Realty

Steve Peckar • Matt Landes

Peter Kapurnais • Garth Gibbons

JLL

Pat Stucker • Ray White • Travis Hodge

Cushman & Wakefield

Pat Henry

Interurban Corporation

William T. Doogan

ARA – A Newmark Company

Jeff Hawks • Doug Andrews • Terrance Hunt

Shane Ozment • Chris Cowan • Steve O’Dell

Justin Hunt • Andy Hellman • Saul Levy

Kevin McKenna • Jessica Graham

Spencer Bradley • Robert Bratley

Anna Stevens • Amanda Meldrum

Julie Rhoades • Kevin Jewett

Colorado Group, Inc.

Miles King • Scott Crabtree

Jessica Cashmore • Todd Walsh

CBRE

Dave Potarf • Dan Woodward

Matthew Barnett • Jake Young

Colliers International

Craig Stack • Bill Morkes

Berkadia

Winston Black • John Laratta

MULTIFAMILY BROKER DIRECTORY

For contact information, firm profiles and links, please visit

click on Industry Directory, then Brokers, then Multifamily subcategory

Multifamily Broker Directory

@

W

e’re all aware of what

seems to be a building

frenzy in the apartment

sector in Denver, accom-

panied, until recently, by

strong rent growth. According to

the latest report from apartment

data provider Axiometrics, “Denver

had a similar (to San Francisco)

end to 2015, finishing with its low-

est year-to-date rent growth of the

recovery – though 5.6 percent was

fairly robust,” it said. “Things were

looking the same through the first

two months of 2016, with negative

YTD rent growth in January, though

a strong March rebound moved it

out of the post-recession basement.”

And here are some nuggets from

the quarter-one market perfor-

mance summary on the Denver,

Aurora and Lakewood metropolitan

statistical area:

• The market’s annual rent growth

rate was above the national average

of 4.1 percent.

• The market’s occupancy rate

decreased from 94.7 percent in

fourth-quarter 2015 to 94.5 percent

in first-quarter 2016.

• As of April 10, Axiometrics iden-

tified 9,056 apartment units sched-

uled for delivery in 2016, of which,

1,958 have been delivered. As a

comparison, there were 9,197 apart-

ment units delivered in 2015. Prop-

erties delivered to the market in the

last 12 months achieved an average

asking rent of $1,816 per unit. Effec-

tive rent has averaged $1,753.

So there is a snapshot of the

recent past, which seems to indi-

cate continued construction in the

face of only mildly

softening (by grow-

ing more slowly)

building perfor-

mance. But what

do the long-term

trends look like?

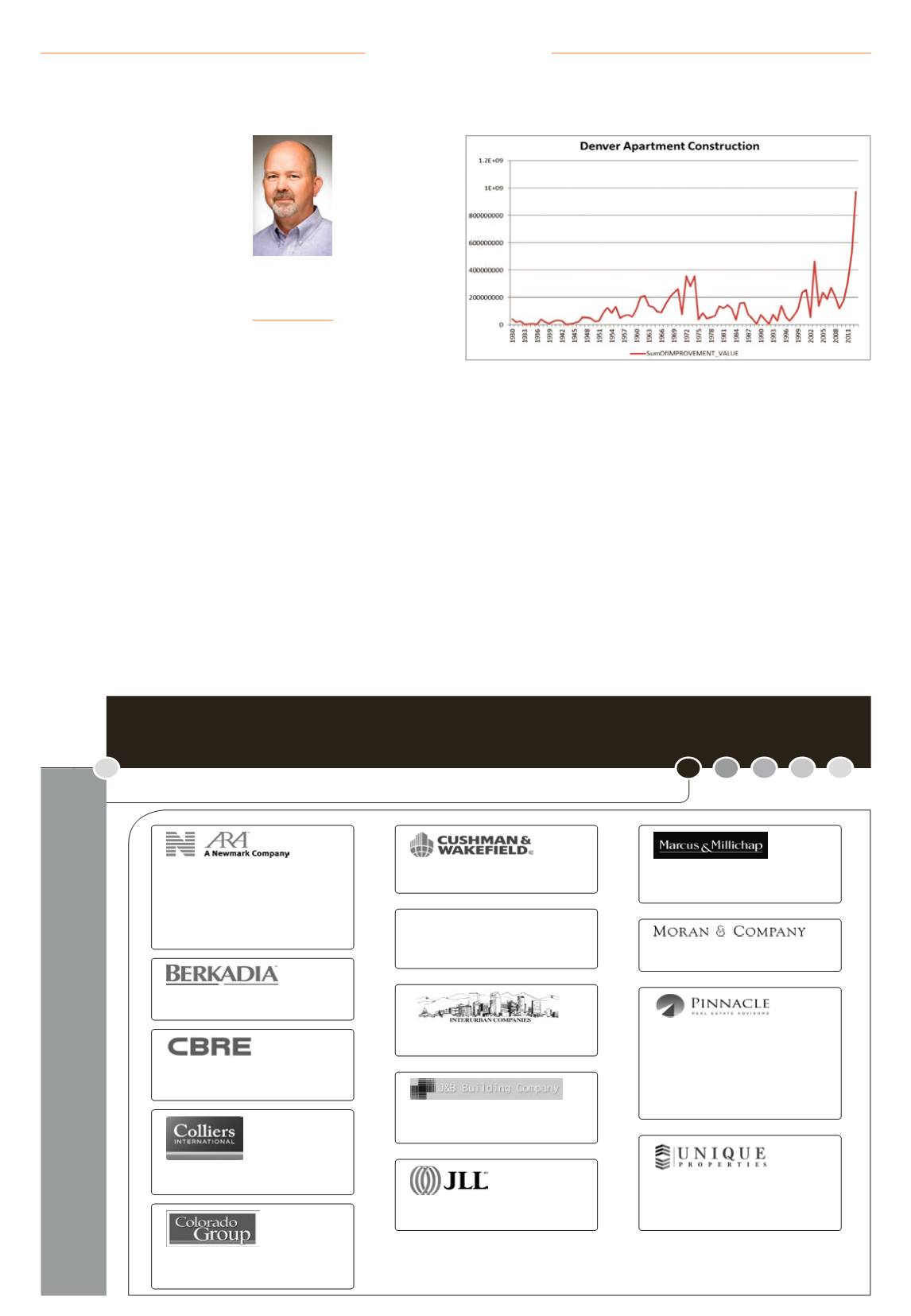

Historical

Perspective

By long term I’m

not talking about

the 1980s, but rath-

er everything built

since the Great

Depression. How

did Denver grow and what were the

trends into and out of and back into

the urban core, Englewood or Lower

Downtown?

All markets go through construc-

tion cycles, and we only think this

one is particularly noteworthy

because we are in it. The chart

seems to bear this out; however,

there is a very noticeable uptick

when you look at what has hap-

pened since 2011.

The vertical axis in this case is

the total current appraised value

of the properties originally built

in each year and comes from the

Denver Assessor’s Office, which

lacks much detail for recent years,

but the report from Axiometrics

suggests this upward trend contin-

ued through the peak of deliveries,

which was just last year (in units).

In the 1930s, 1940s and 1950s,

multifamily construction activity

in Denver was fairly widespread.

Of course, this is a 30-year period,

but there were several pockets of

concentration as opposed to one

dominant area – the latter of which

is common in many metro areas in

this time frame.

The ’60s follow a similar pattern

with a little less dispersion and

more concentration downtown and

south, but the ’70s, ’80s and ’90s

show fairly dispersed activity with

no one highly favored area of con-

centration.

This changes in the early 2000s,

when a building boom begins to

take a foothold in the LoDo area,

with other areas of concentration

south of downtown. This 2000 to

2009 period represents 91 apart-

ment buildings over $3 million in

current appraised value, includ-

ing mixed-use. In the 1990s, that

number was only 24. This trend has

become even more pronounced in

the years since 2010. You can view

a video of the entire progression by

decade on our website, where there

also is a video showing this same

information annually for 2000 –

2015.

Returning to long-term trends –

there’s no question we are building

a historically unseen level of apart-

ments and at volumes multiples

beyond previous periods. Rents

seem to be softening some, but will

continue to be driven by supportive

demographics and job growth. That

being said, job growth is cyclical and

highly correlated to rent growth.

Mark Daniel

Vice president,

partner relations,

RealMassive,

Austin

Final Thoughts

Graphic courtesy RealMassive

While all markets go through construction cycles, the current cycle is producing at

historic rates.