Page 20

— Multifamily Properties Quarterly — October 2015

C

oming out of the recession, the

Denver multifamily market began

an incredible run of rent gains –

a streak so unprecedented that

the only thing Denverites have to

compare it with is the Colorado Rock-

ies improbable push

to the 2007World

Series. In January

2010, average effec-

tive rent for the

Denver metropolitan

statistical area was

$828, according to

Axiometrics.Today,

that number is

$1,364 – an increase

of nearly 65 percent

over five years.

Median household

income, however,

has been on a dif-

ferent trajectory. In

2014, MHI for Denver

was $66,870, accord-

ing to U.S. Census.

Compare this with

a MHI of $58,732 in

2010, which pres-

ents an increase of

just under 14 per-

cent.The difference

between 65 percent

and 14 percent is

monumental.

The gap between

rent growth and

income growth

resulted in a flight

to affordability in

metro Denver, with

Class C apartments

being the beneficiary.

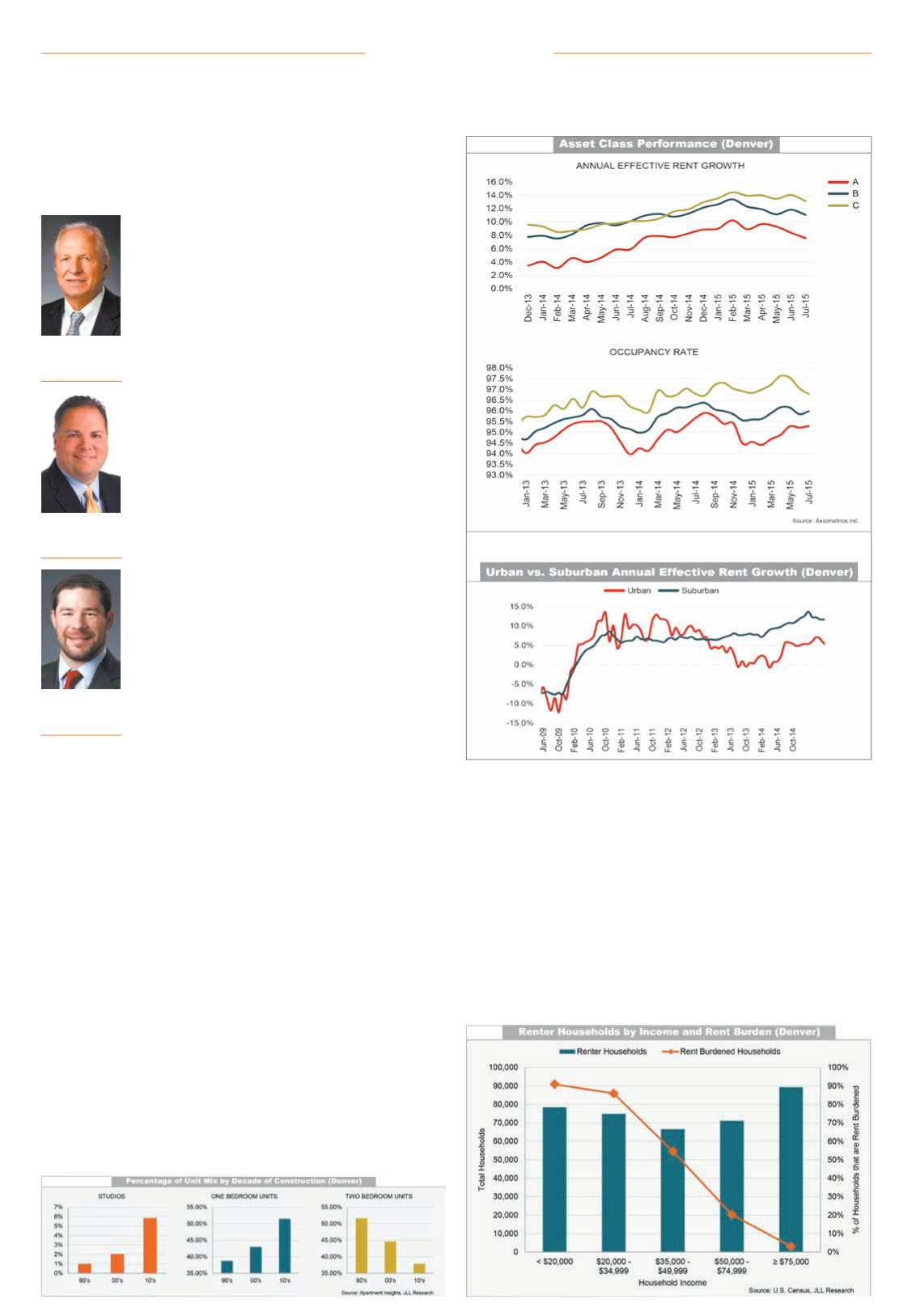

Annual effective rent

growth for Class C

properties is 13.1

percent, which is

higher than Class

B, 11.1 percent, and

Class A, 7.6 percent.

Occupancy tells a similar story, with

Class C at 96.8 percent, which is higher

than Class B at 96 percent and Class A

at 95.3 percent.The difference in per-

formance between urban and the less

expensive suburban properties adds

further evidence, with 11.7 percent

annual rent gains for suburban proper-

ties, which is more than double the 5.4

percent for urban properties.

It’s clear that the issue of affordabil-

ity is having an impact on the rental

market, which raises the question: How

will today’s pricing affect tomorrow’s

supply? It’s an important question for

property owners and developers.

Looking at historical unit mix

trends, we can see that developers are

responding by building smaller units.

From the 1990s to the current decade,

developers have increased the percent-

age of studios built six-fold. Over each

of the last three decades, we’ve seen

the percentage of two-bedroom units

decline while studios and one-bedroom

units increased.

Digging a little deeper, we can pin-

point some notable examples of this

shift. Denver’s central business dis-

trict, the submarket with the highest

average rent per unit, has responded

accordingly – 73 percent of units deliv-

ered since 2013 have been studios and

one-bedroom units, according to Apart-

ment Insights.

The Denver Tech Center followed

suit; in 2014 and 2015, the DTC saw six

projects deliver 60 percent studios and

one-bedroom units. Of those six, two

projects stood at 70 percent studios

and one bedrooms, with another top-

ping out at 80 percent.

Perhaps the most notable example

of this shift isTurntable Studios, which

is a redevelopment of the old Hotel VQ

and Denver’s first project with market-

rate units smaller than 350 square feet.

Micro units (typically ranging from

275 to 400 sf) first started popping up

in high-density, expensive metro mar-

kets like San Francisco, Seattle, Boston,

Washington, D.C., and NewYork, but

today are found in less-likely metros,

such as Des Moines, Iowa, Columbus,

Ohio, and Omaha, Nebraska.

These units typically rent on a

dollars-per-month basis for 20 to 30

percent below conventional units, even

though the rents per sf are much high-

er. From large to small markets, there

is a demand for smaller units. It’s a

price-point play for many renters, and

it’s clear that the issue of affordability

reaches well beyond Denver.

WhileTurntable Studios is the first of

its kind in Denver, it certainly won’t be

the last.This is a new trend, so natu-

rally there are skeptics questioning

the exit for micro-unit investments 10

years down the road. However, even if

rent-to-income ratios in Denver regress

to 2010 levels, the migration is clear;

the demand for affordable units will

drive occupancy for micro units from a

price-point perspective.

According to the 2014 Urban Land

Institute report, “The MacroView on

Micro Units,” a survey of micro-unit

renters showed 86 percent of respon-

dents indicated price as a priority in

the initial leasing decision. Additionally,

24 percent of respondents from a sur-

vey of conventional unit renters indi-

cated they would be interested or very

interested in renting a micro unit with

73 percent of respondents ranking price

as the No. 1 or No. 2 reason they would

choose a micro unit over conventional.

It’s clear that many renters see an

economic benefit to micro units, but

also developers are economic benefi-

ciaries. Because of the relatively fixed

cost linked to kitchens and bathrooms,

micro-unit projects cost 5 to 10 percent

more per sf to develop than conven-

tional projects; however, the 25 percent

price per sf rent premiummicro units

typically achieve more than offsets the

added cost.

As the number of micro-unit projects

grows, developers are creating a new

market and value network – two key

components of disruptive innovation –

for lower-income renters.That’s not to

suggest that one day new construction

will consist of only micro units; rather,

we should expect a greater diversity

in housing options moving forward

as projects with smaller units help

combat market affordability concerns.

“Affordability” is a relative term, howev-

er, and can be applied to high-income

households as well.

According to the U.S. Census 2014

American Community Survey, 30.8 per-

cent of households in the metro Den-

ver area have incomes of $100,000 or

greater, ranking Denver 25th out of 381

MSAs for the highest percentage. Fall-

ing below Denver’s 25th spot are MSAs

such as Los Angeles, Miami, Philadel-

phia and Chicago – markets where the

portion of households earning $100,000

or more is smaller than in Denver, yet,

according to Axiometrics, effective

rents are anywhere from $115 to $795

per month higher than in Denver.

Additionally, the 2014 ACS breaks

down Denver’s renter households into

segments based on household income,

with the highest income segment being

households earning $75,000 or more.

Households in this segment outnum-

ber lower-income segments, making up

22.5 percent of all renter households. Of

the renter households earning $75,000

or more, only 3 percent are described

as rent burdened (households contrib-

uting 30 percent or more of income

toward rent), the lowest percentage of

any household income segment.

With all the talk over rents getting

too high, there’s still a sizable portion

of the rental market readily equipped

to absorb higher rents.This, of course,

is good news for developers and inves-

tors, as there’s a wide range of invest-

ment options, from the lower end of

the market micro units to the upper-

end Class A core.

s

Market Drivers

Pat Stucker

Managing director,

JLL, Denver

Ray White

Vice president,

JLL, Denver

Travis Hodge

Associate,

JLL, Denver

Charts courtesy JLL