Page 6

— Health Care Properties Quarterly — June 2016

D

enver’s medical office mar-

ket remains healthy, accord-

ing to recent reports noting

improvements in construc-

tion activity, investment

activity and rental rates.

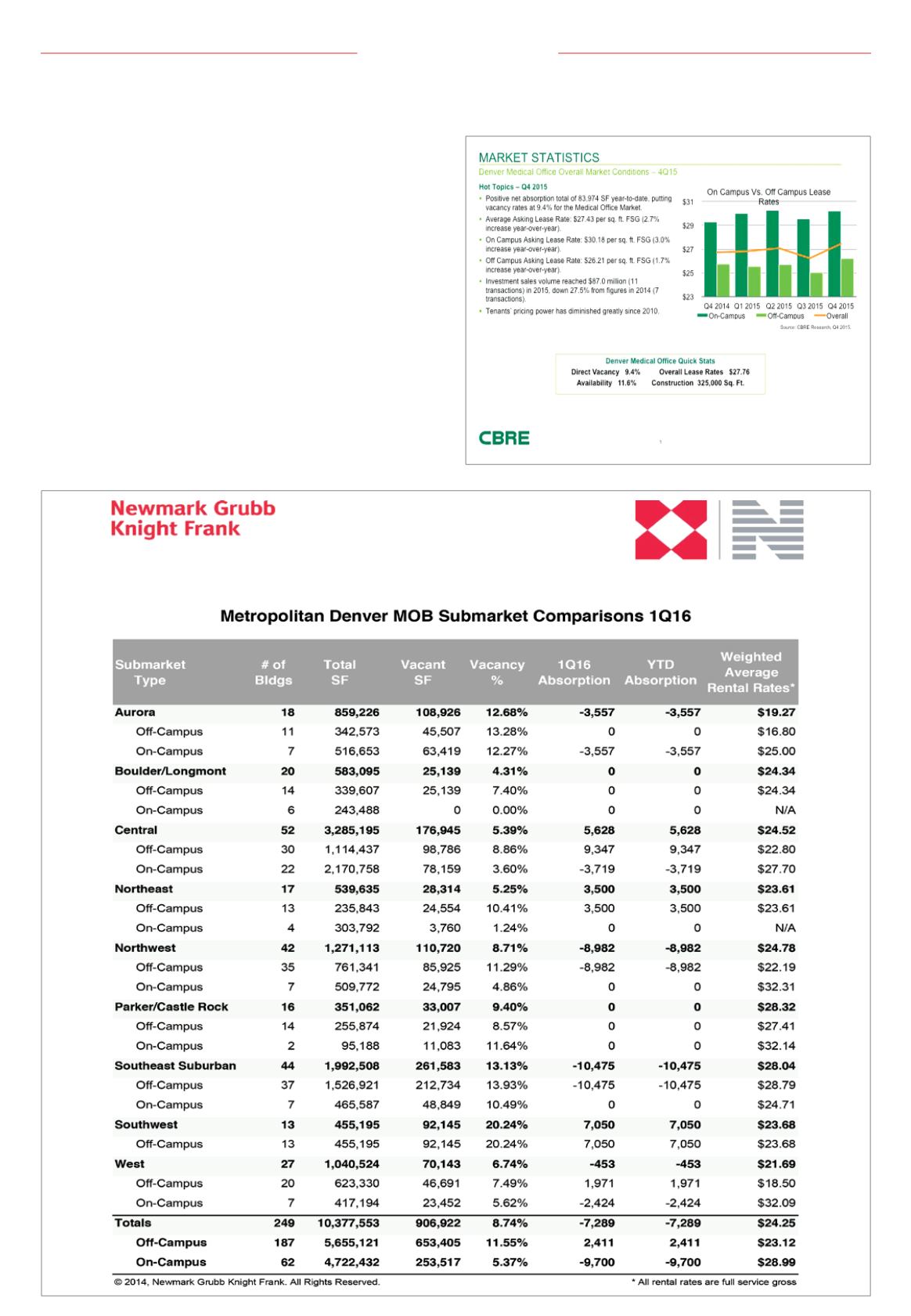

CBRE’s most recent report, from

fourth-quarter 2015, noted that the

average direct asking lease rate

increased to $27.34 per square foot

full service gross quarter over quar-

ter, representing an increase of 3.1

percent year over year. The reported

also noted that overall direct vacan-

cy decreased to 9.6 percent in the

quarter – a 19 basis point increase

year over year.

Additionally, construction activity

ended the year at 325,000 sf.

Investment sales ended 2015 with

$87 million transacted. CBRE expects

an increase in transaction volume in

2016, pushing activity to 2014 levels

when more than $120 million was

closed.

“Strengthening fundamentals and

continued economic progress will

afford new opportunities to upgrade

the health care system, allowing

investors and lenders to drive trans-

action levels up,” according to CBRE.

NewMark Grubb Knight Frank’s

first-quarter 2016 medical office

building submarket report noted

that total vacancy was 8.74 percent

with on-campus properties ending

the first three months of the year

with a 5.37 percent vacancy fig-

ure. The central submarket, metro

Denver’s largest medical office

submarket with 3.29 million sf in

52 buildings, had one of the lowest

vacancy rates of all the submarkets

surveyed at 5.39 percent. The high-

est weighted average rental rates

(full service gross) were seen in the

Parker/Castle Rock submarket with

a rate of $28.32. Overall weighted

average rental rates ended the quar-

ter at $24.25 across the metro area,

with on-campus properties averag-

ing $28.99 versus $23.13 to their off-

campus counterparts.

s

Market Update