Page 16B—

COLORADO REAL ESTATE JOURNAL

—

September 2-September 15, 2015

an all-in cost of $160,000 to

$170,000 per unit. The same

developments, in our current

construction environment,

cost from $200,000 to $210,000

per unit, which dramatically

changes developers’ proformas.

While skyrocketing rents

in prime metro Denver

submarkets easily will justify the

increased cost and subsequent

development, many will stall

before shovels are put in the

ground.

However, the increased

timelines and costs have

not discouraged seasoned

developers. In many cases,

developers are charging forward

but resigning to the fact that

timelines and budgets are

simply outside of their control.

“Construction costs and

timelines have increased

significantly,” said Andy

Mutz, senior vice president

at AMLI. “We are working to

address these concerns for

our developments, but the

marketplace is driving the ship

right now.”

Undoubtedly, the most critical

influence to Denver’s apartment

pipeline is the flow of equity

investment that allows proposed

developments to go vertical. It is

an open spigot, but will quickly

run dry if Denver’s record-

breaking absorption statistics

slow. Big money is begging to

be spent in Denver, but many

investors are holding their

breath in anticipation of the

next quarterly market report to

validate continued investment.

Well-planned developments

still make sense in the metro

area. The unmet demand for

apartments has yet to be satiated

due to Colorado’s in-migration

and absorption. Slower

timelines and financial hurdles

for development mean Denver’s

vacancy rate will remain

manageable. If the current

construction pipeline progresses

as we expect, and absorption

slowly tapers, vacancy could end

up at about 6 percent in 2018.

Of course, there is always

construction defect reform

that could impact Denver’s

apartment market, but that is a

topic for another day.

replaced by hours on market.

With such demand, the supply

of finished lots has reached

historic lows. So one would

think there are several new

residential developments under

construction or being planned.

However, that is not the case.

Many new projects are on

hold due to the price of water.

Traditionally, municipalities

require 3 acre-feet of water

for each acre of land. When

raw water was $10,000 per

acre-foot this was doable. But

at over $50,000 per acre-foot,

the numbers barely work for a

$400,000 house and definitely

don’t work for a starter home.

Entry-level homes of $250,000

are history. There are few home

sites remaining for less than

$60,000 in Northern Colorado.

Affordability is gaining much

attention in both Larimer and

Weld counties.

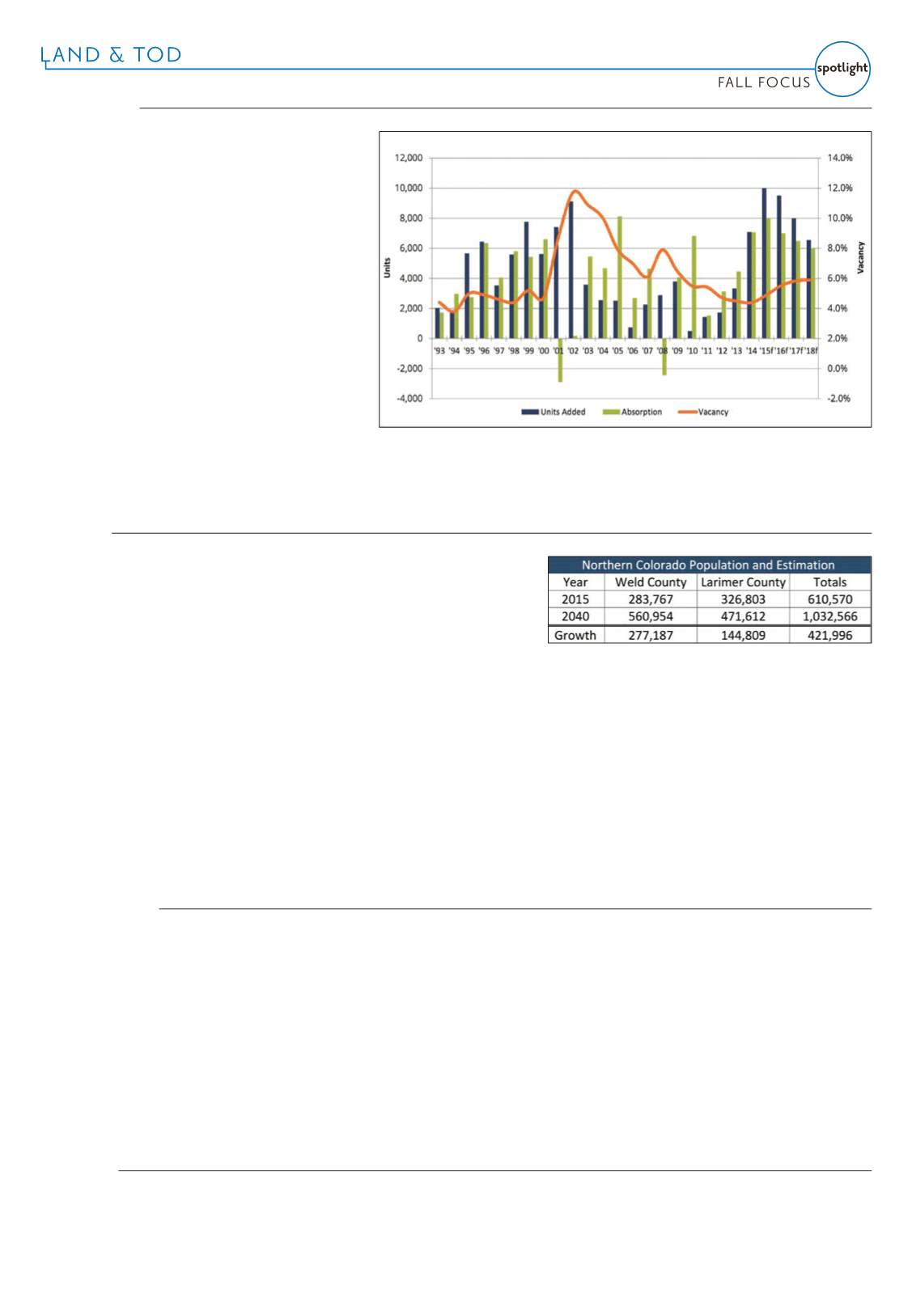

Apartments.

In 2009, less

than 50 units were permitted

in the Fort Collins metro area.

But over the next three years,

an average of 525 units were

permitted. Then in 2013, nearly

1,000 units were permitted with

an additional 925 units in final

planning. Student housing

for CSU has been the major

focus. Newly completed projects

adjacent to the university

added over 1,900 beds with an

additional 2,100 beds nearing

completion. Currently, four

planned projects could add

another 1,400 beds. Pricing for

land ranges from $12,000 to

$15,000 per unit for the larger

projects having densities of

fewer than 20 units per acre.

Retail.

Demand is strong for

the “100 percent” locations. In

these projects, land prices for

1-acre sites are approaching $20

per sf. Following are examples of

retail anchors at “100 percent”

shopping center locations.

• A 250,000-sf Scheels at

Interstate 25 and U.S. Highway

34 in Loveland;

• Target, Safeway and Kohl’s at

Centerplace of Greeley in west

Greeley;

• Discount Tire, Kum & Go,

general retail and restaurants

at St. Michael’s Town Square in

west Greeley; and

• Walmart and Costco at I-25

and Harmony Road in Timnath

near Fort Collins.

Outside of these

developments, there has been

little new retail. Asking prices for

commercial sites have escalated

but there have been few actual

sales.

Industrial.

In 2013 and 2014,

oil and gas businesses servicing

the exploration and production

of the Niobrara shale formation

were desperate for industrial

properties, especially in or

near the Highway 85 corridor.

Building rents quickly rose from

$5 per sf to $15 or more per sf

and the few developed industrial

lots were quickly absorbed. But

for the most part, price increases

were muted, rising from the

$2.50 to $3.50 per sf range.

Water.

Prices have quadrupled

over the last three years driven

by the heightened post-recession

growth in the Northern Front

Range plus the expansion of

the oil and gas industry. With

limited new water storage

facilities coming on line in the

near term, prices will continue

to rise. Right now the most

important issue is water – for all

of Colorado.

Colorado likely will add 1

million-plus people over the

next 20 years with most locating

in the Front Range. In terms

of the demand for land, the

prospects are nothing short of

excellent, long term. There will

be more booms and more busts

but the trend line is strongly

positive.

incorporates trail connections

and opportunities for recreation,

as well as a health and wellness

education plan that must be kept

current.

Imperative No. 10, resilient

community connections,

includes strategies that foster

resiliency through infrastructure,

planning and communication. It

states that a secure shelter must

be provided for 100 percent of

the residents to congregate in

an emergency situation. Backup

generators must be provided for

all facilities, in addition to single-

family residences, and sensitive

infrastructure must be kept out

of the flood plain. Community

safety is cultivated through the

use of a neighborhood watch

program, and disaster response

plans must be disseminated

with trained and assigned block

captains.

The marriage between

community and resiliency

is key to enabling the built

environment to rebound

effortlessly, as nature does, and

the LCC will make great strides

in building this connection.

Staying true to the

commitment of sharing

knowledge, IFLI provided

pattern language tools, which

are meant to serve as a starting

point for project teams, and

invited others to submit their

own patterns to share. The two

that are available now are “San

Francisco Living Community

Patterns,” developed by the San

Francisco Planning Department

and ILFI, and “Child-Centered

Planning: A New Specialized

Pattern Language Tool,”

developed by Jason McClellan. A

few examples of these patterns

include urban rewilding and

blue green streets, which

marry vegetation and water

treatment, grower/maker spaces

and unstructured play where

children can interact with the

environment like they would

in nature, encouraging a sense

of exploration and need for

tactile investigation. The guides

also provide valuable real-world

case studies that showcase the

patterns in use.

The Living Community

Challenge is not for the faint of

heart or those content with the

status quo. It is for visionaries

– those who see the potential

of what could be and those

who decide to do today what

could be put off until tomorrow.

In Jason McClellan’s article

“Cities Are Now,” published in

the winter 2015 issue of Yes!

Magazine, he stated, “Human

behavior is shaped in large

part by our ability to pursue

what we can imagine.” The

Living Community Challenge

provides a vision. Luckily, ILFI

also provides research, resources

and current pilot cases, which

demonstrate that this is not just a

pipe dream.

land use and water planners in

the next few years.

It is clearly just the beginning

of the land use and water

planning conversation. The

Keystone Policy Center

also is trying to move the

conversation along through

its Colorado water and growth

dialogue program. Since

early 2014, the dialogue has

convened meetings of 25

individuals from the land and

water planning fields as well

as economic development

organizations. The purpose is

to identify land use patterns

and incentives that will save

water and still deliver housing

products that consumers

find attractive, said Matthew

Mulica of the Keystone Center,

who is leading the effort.

Having actual, comparable

data about growth and its

water use implications could

help overcome some of the

disconnect between water

providers and planning

departments.

Mulica points to the central

reality that Colorado has a

zero-sum water game. “We

are going to have to set some

priorities and make some

choices, and do it in smart,

strategic ways,” said Mulica.

For more information, visit

the Colorado Foundation for

Water Education website and

Headwaters magazine at www.

yourwatercolorado.org.

Denver’s current construction pipeline graph and prediction for the next few years