6 / 24

6 / 24

Page 6

— Health Care Properties Quarterly — October 2017

www.crej.comMarket Update

D

enver’s medical office

building market remains

an attractive niche with

solid fundamentals in the

first half of 2017 due to

strong demand for quality space

and favorable demographic trends,

according to a recent report on the

metro area’s medical office market.

CBRE’s report on the first half of

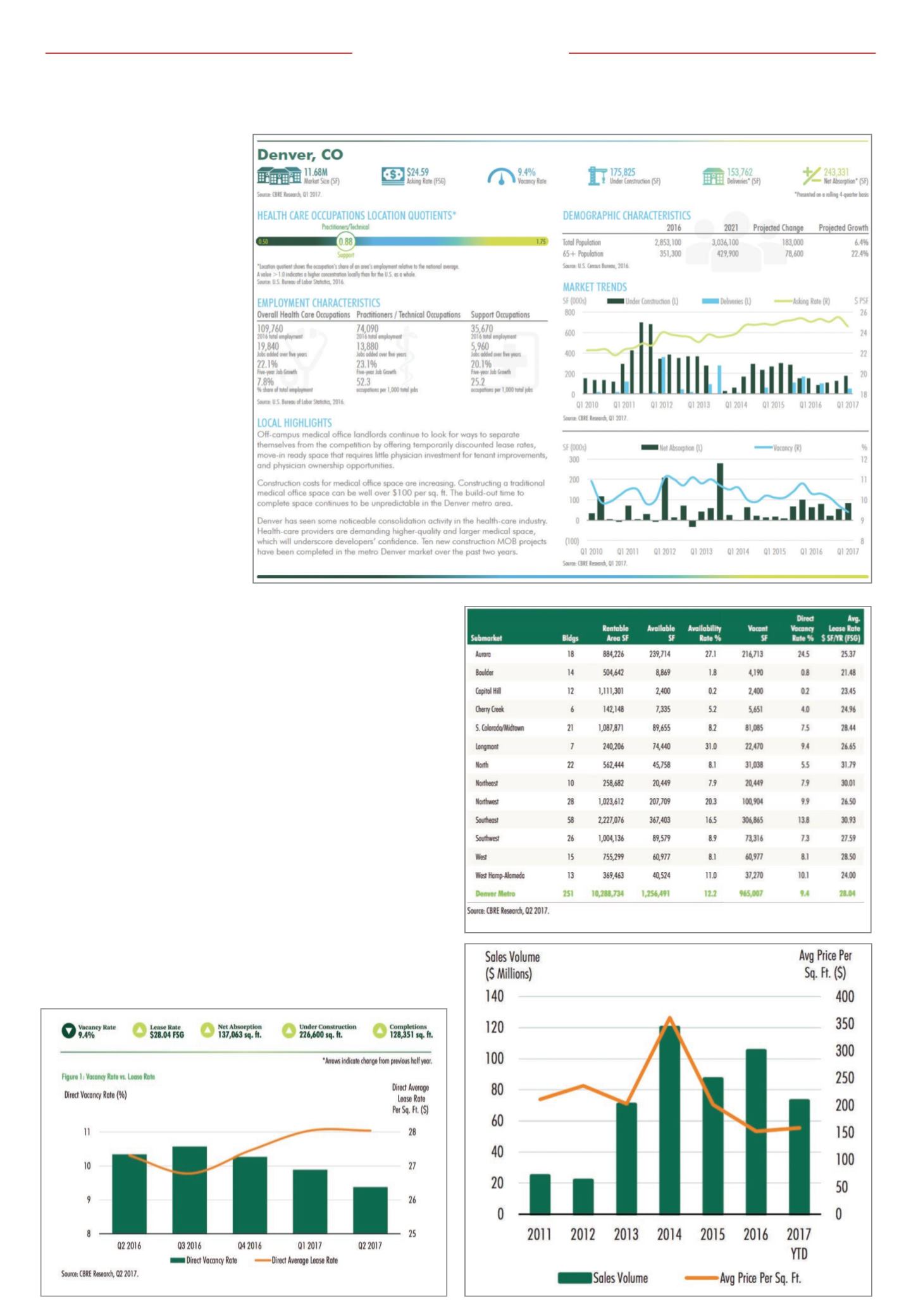

2017 noted that Denver’s overall

vacancy rate decreased to 9.4 per-

cent, down 96 basis points year

over year.

The decline in vacancy rate is

mirrored in the overall U.S. medi-

cal office vacancy rate, which was

8 percent, according to CBRE’s look

at the national medical office mar-

ket. The decline is seen from the

growth in the aging U.S. population,

pressure for health care providers

to cut costs and new technologies

boosting demand for medical office

properties in recent years.

“The steep increase in the 65-plus

population and anticipated greater

need for in-office physician servic-

es by this group signals a continued

increase in demand for health care

services and medical office space

in the years ahead,” said Andrea

Cross, Americas head of office

research, CBRE.

Within the Denver medical office

market, a positive net absorption of

41,091 square feet was recorded in

the second quarter, bringing year-

to-date absorption to 137,063 sf – a

41.6 percent increase compared

with second-half 2016.

CBRE noted that off-campus

medical buildings have gained in

popularity, posting positive net

absorption in the last two quarters.

The growth in off-campus MOBs

is partially due to lower rent and

future ownership opportunities.

Overall availability remains stable

in recent quarters, ending the sec-

ond quarter at 12.2 percent, with

off-campus availability at 13.4 per-

cent and on-campus availability at

10 percent.

The report noted that the aver-

age direct asking lease rate was

$28.04 per sf full service gross at

the end of the second quarter – a

2.7 percent uptick year over year.

The off-campus average direct leas-

ing rate rose to $27.22 per sf, up 87

cents per sf year over year while

the on-campus average rate stood

at $29.03 per sf. For comparison,

the average direct asking lease rate

for general office space in metro

Denver was $26.15 per sf FSG.

The Denver MOB market contin-

ues to experience strong levels of

construction activity, according to

the report, with 226,600 sf under

construction at the end of the sec-

ond quarter. Construction costs are

increasing due to the rising cost

of materials and a labor shortage,

however, are still lower than many

parts of the United States.

Investors also remain interested

in the Denver medical office mar-

ket, reflected in “robust” invest-

ment activity during the first half

of 2017. There has been $72.8 mil-

lion in transaction volume year to

date, up 87.6 percent from first-half

2016.

“As investor appetite for health

care-related real estate has grown,

medical office buildings have

emerged as the most popular type

within the sector,” Chris Bodnar,

executive vice president, Health-

care, CBRE Capital Markets, said

of the overall U.S. medical office

market. “As yields for traditional

real estate asset classes have

compressed in recent years, new

capital sources, including foreign

capital, have entered the medical

office sector in search of stability to

hedge against any potential correc-

tion in the global markets.”

▲

Denver’s medical office market remains attractive